EXHIBIT 99.1

Published on January 14, 2020

Exhibit 99.1

Investor Presentation January 2020

2 Forward Looking Statements This presentation contains forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 , Section 27A of the Securities Act and Section 21E of the Exchange Act, such as statements about the transactions described herein, includ ing the ability of Apollo Medical Holdings, Inc. and its subsidiaries and variable interest entities (the “Company” or “ApolloMed”) to raise the funding necessary to consummate the transactions, management’s view of the future expectations and prospects for the Company and the fin ancial and non - financial benefits expected to be received from the transactions. Forward - looking statements include any statements abou t the Company's business, financial condition, operating results, plans, objectives, expectations and intentions, and any projectio ns of earnings, revenue or other financial items, such as the Company's projected capitation and future liquidity, and may be identified by t he use of forward - looking terms such as “anticipate,” “could,” “can,” “may,” “might,” “potential,” “predict,” “should,” “estimate,” “expec t,” “project,” “believe,” “plan,” “envision,” “intend,” “continue,” “target,” “seek,” “will,” “would,” and the negative of such t erm s, other variations on such terms or other similar or comparable words, phrases or terminology. Forward - looking statements reflect curren t views with respect to future events and financial performance and therefore cannot be guaranteed. Such statements are based on the curre nt expectations and certain assumptions of the Company's management, and some or all of such expectations and assumptions may no t materialize or may vary significantly from actual results. Actual results may also vary materially from forward - looking statemen ts due to risks, uncertainties and other factors, known and unknown, including the risk factors described from time to time in the Comp any 's reports to the U.S. Securities and Exchange Commission (the “SEC”), including without limitation the risk factors discussed in the Compa ny' s Annual Report on Form 10 - K filed with the SEC on March 18, 2019 and subsequent 10 - Q filings. Because the factors referred to above could cause actual results or outcomes to differ materially from those expressed or imp lie d in any forward - looking statements, you should not place undue reliance on any such forward - looking statements. Further, any forward - loo king statement speaks only as of the date of this presentation and, unless legally required, the Company does not undertake any ob lig ation to update any forward - looking statement, as a result of new information, future events or otherwise.

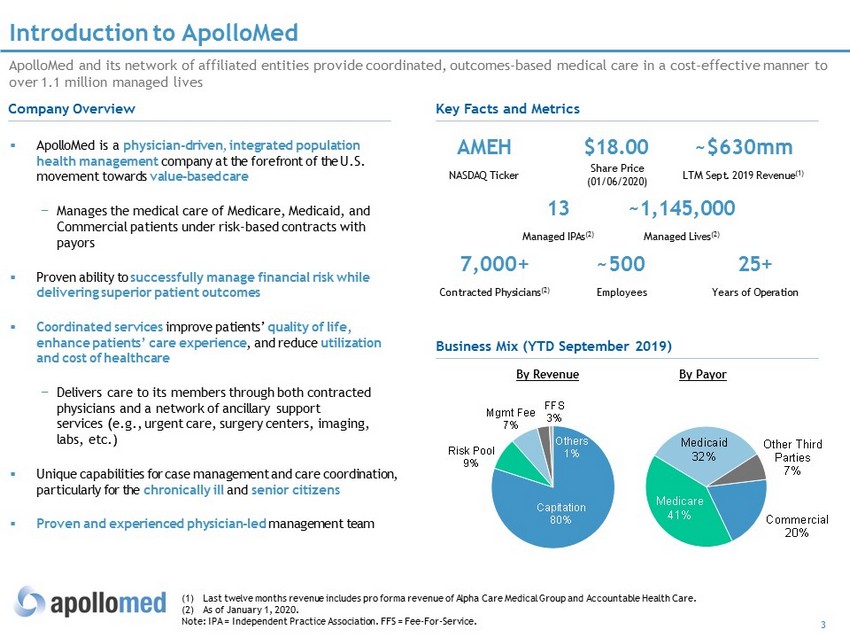

3 Introduction to ApolloMed (1) Last twelve months revenue includes pro forma revenue of Alpha Care Medical Group and Accountable Health Care. (2) As of January 1, 2020. Note: IPA = Independent Practice Association. FFS = Fee - For - Service. ApolloMed and its network of affiliated entities provide coordinated, outcomes - based medical care in a cost - effective manner to over 1.1 million managed lives ▪ ApolloMed is a physician - driven , integrated population health management company at the forefront of the U.S. movement towards value - based care − Manages the medical care of Medicare, Medicaid, and Commercial patients under risk - based contracts with payors ▪ Proven ability to successfully manage financial risk while delivering superior patient outcomes ▪ Coordinated services improve patient s’ quality of life, enhance patients’ c a re experience , and reduce utilization and cost of healthcare − Delivers care to its members through both contracted physicians and a network of ancillary support services (e.g., urgent care, surgery centers, imaging , labs, etc .) ▪ Unique capabilities for case management and care coordination , particularly for the chronically ill and senior citizens ▪ Proven and experienced p hysician - led managemen t team Key Facts and Metrics AM E H N AS D A Q Tic ke r $1 8.00 S h a r e P r ic e (01/06/2020) ~ 1,145 , 00 0 Ma n a ge d L iv e s (2 ) 1 3 Ma n a ge d I P A s (2) ~ 5 00 E m p lo yee s 7 , 000 + C o nt r ac te d P hy s icia n s (2 ) Business Mix (YTD September 2019) Commercial 20% Medicare 41% Medicaid 32% Other Third Parties 7% 25+ Years of Operation ~$630mm LTM Sept. 2019 Revenue (1) Capitation 80% Risk Pool 9% Mgmt Fee 7% FFS 3% Others 1% By Revenue By Payor Company Overview

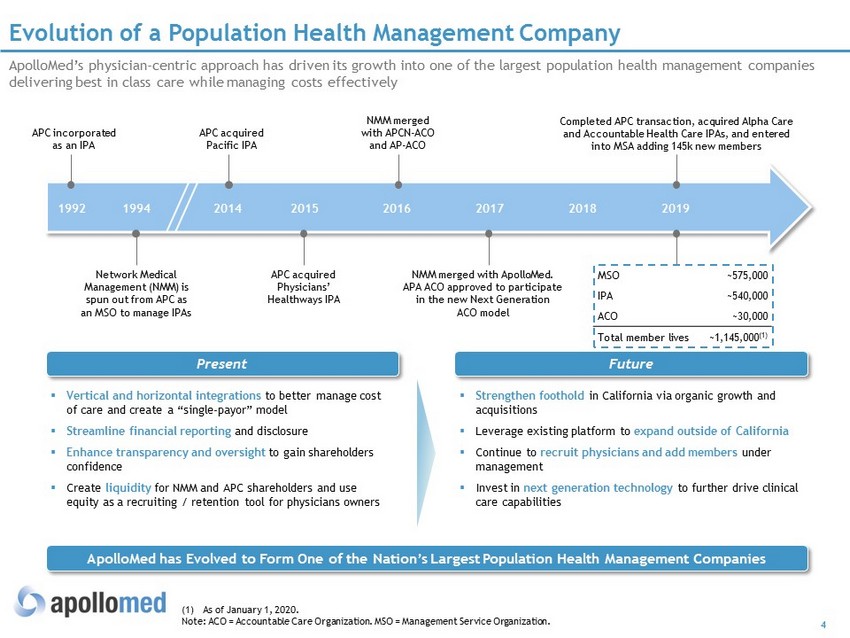

4 MSO ~575,000 IPA ~540,000 ACO ~30,000 Total member lives ~1,145,000 (1) Evolution of a Population Health Management Company ApolloMed’s physician - centric approach has driven its growth into one of the largest population health management companies delivering best in class care while managing costs effectively (1) As of January 1, 2020. Note : ACO = Accountable Care Organization. MSO = Management Service Organization . APC incorporated as an IPA 1992 1994 Network Medical Management (NMM) is spun out from APC as an MSO to manage IPAs 2014 APC acquired Pacific IPA APC acquired Physicians’ Healthways IPA 2015 2016 2017 2018 2019 NMM merged with APCN - ACO and AP - ACO NMM merged with ApolloMed. APA ACO approved to participate in the new Next Generation ACO model Present Future ▪ Vertical and horizontal integrations to better manage cost of care and create a “single - payor” model ▪ Streamline financial reporting and disclosure ▪ Enhance transparency and oversight to gain shareholders confidence ▪ Create liquidity for NMM and APC shareholders and use equity as a recruiting / retention tool for physicians owners ▪ Strengthen foothold in California via organic growth and acquisitions ▪ Leverage existing platform to expand outside of California ▪ Continue to recruit physicians and add members under management ▪ Invest in next generation technology to further drive clinical care capabilities ApolloMed has Evolved to F orm One of the Nation’s Largest Population Health Management Companies Completed APC transaction, acquired Alpha Care and Accountable Health Care IPAs, and entered into MSA adding 145k new members

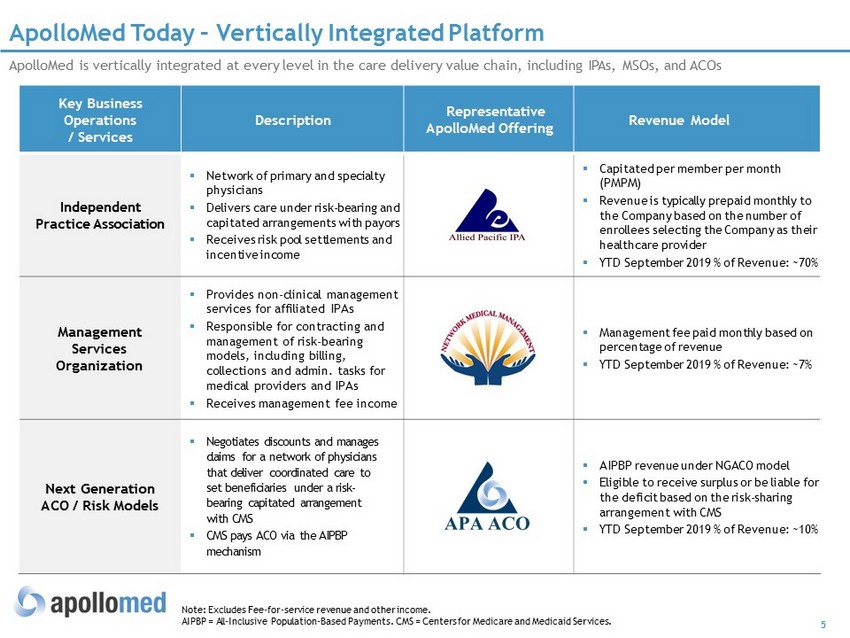

5 Key Business Operations / Services Description Representative ApolloMe d Offering Revenue Model Independent Practice Association ▪ Network of primary and specialty physicians ▪ Delivers care under risk - bearing and capitated arrangements with payors ▪ Receives risk pool settlements and incentive income ▪ Capitated per member per month (PMPM) ▪ Revenue is typically prepaid monthly to the Company based on the number of enrollees selecting the Company as their healthcare provider ▪ YTD September 2019 % of Revenue: ~70% Management Services Organization ▪ Provides non - clinical management services for affiliated IPAs ▪ Responsible for contracting and management of risk - bearing models, including billing, collections and admin. tasks for medical providers and IPAs ▪ Receives management fee income ▪ Management fee paid monthly based on percentage of revenue ▪ YTD September 2019 % of Revenue: ~7% Next Generation ACO / Risk Models ▪ Negotiates discounts and manages claims for a network of physicians that deliver coordinated care to set beneficiaries under a risk - bearing capitated arrangement with CMS ▪ CMS pays ACO via the AIPBP mechanism ▪ AIPBP revenue under NGACO model ▪ Eligible to receive surplus or be liable for the deficit based on the risk - sharing arrangement with CMS ▪ YTD September 2019 % of Revenue: ~10% ApolloMed Today – Vertically Integrated Platform ApolloMed is vertically integrated at every level in the care delivery value chain, including IPAs , MSOs , and ACOs Note: Excludes Fee - for - service revenue and other income. AIPBP = All - Inclusive Population - Based Payments . CMS = Centers for Medicare and Medicaid Services.

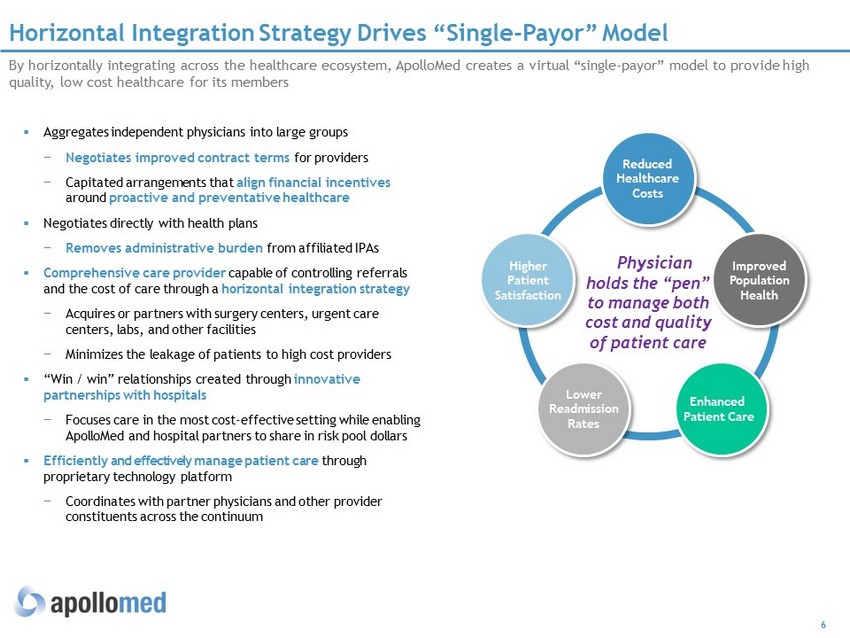

6 Horizontal Integration Strategy Drives “ Single - Payor ” Model By horizontally integrating across the healthcare ecosystem, ApolloMed creates a virtual “ single - payor ” model to provide high quality, low cost healthcare for its members Reduced H ea l t h ca r e Costs Improved P op u l a t i on Health Enhanced Patient Care Higher Patient S a t i s f ac t i on Lower R ea d m i ss i on Rates ▪ Aggregates independent physicians into large groups − Negotiates improved contract terms for providers − Capitated arrangements that align financial incentives around proactive and preventative healthcare ▪ N egotiat es directly with health plans − R emov es a dministrative burden from affiliated IPAs ▪ Comprehensive care provider capable of controlling referrals and the cost of care through a horizontal integration strategy − Acquires or partners with surgery centers, urgent care centers, labs, and other facilities − M inimizes the leakage of patients to high cost providers ▪ “ Win / win” relationships created through innovative partnerships with hospitals − Focuses care in the most cost - effective setting while enabling ApolloMed and hospital partners to share in risk pool dollars ▪ Ef ficiently and effectively manage patient care through proprietary technology platform − Coordinates with partner physicians and other provider constituents across the continuum Physician holds the “pen” to manage both cost and quality of patient care

7 Creating a Next Generation Integrated Healthcare Platform ApolloMed continues to be at the forefront of industry trends towards value - based care and preventative medicine ▪ Participation began January 2017 ; payments commenced April 2017 − ~30,000 Medicare FFS patients currently receiving medical management and care coordination ▪ APA ACO has entered into discounted contracts with participating physicians and preferred providers; in - network Part A and Part B − Responsible for patients’ medical management and payment for all Part A and Part B claims ▪ Only Next Generation ACO in the U.S. operating under all - inclusive population - based payments (AIPBP) − Mo st advanced risk - taking track − CMS remits AIPBP to APA ACO as well as a surplus distribution for earned surplus ▪ Shared risk arrangement whereby shared savings or losses on providing such services are both capped by CMS ▪ CMMI Direct Contracting Model to replace NGACO model beginning 2021 ; Broader reimbursement through total capitation payments for Medicare patients instead of just Part A and Part B ; Stable Cash Flow with benchmarking based on three years of historical FFS spending instead of one year ▪ Robust population health platform designed to manage large populations and encourage patient engagement through a user - friendly care plan wizard and mobile platform: − Personal Digital Care Plans − Predictive and Comprehensive Analytics − Real - time A dmission and Discharge notifications − Telemedicine First - Mover of the Next Generation ACO Continued Investment in the Next Generation Technology and Preventative Care Note: CMMI = Center for Medicare and Medicaid Innovation.

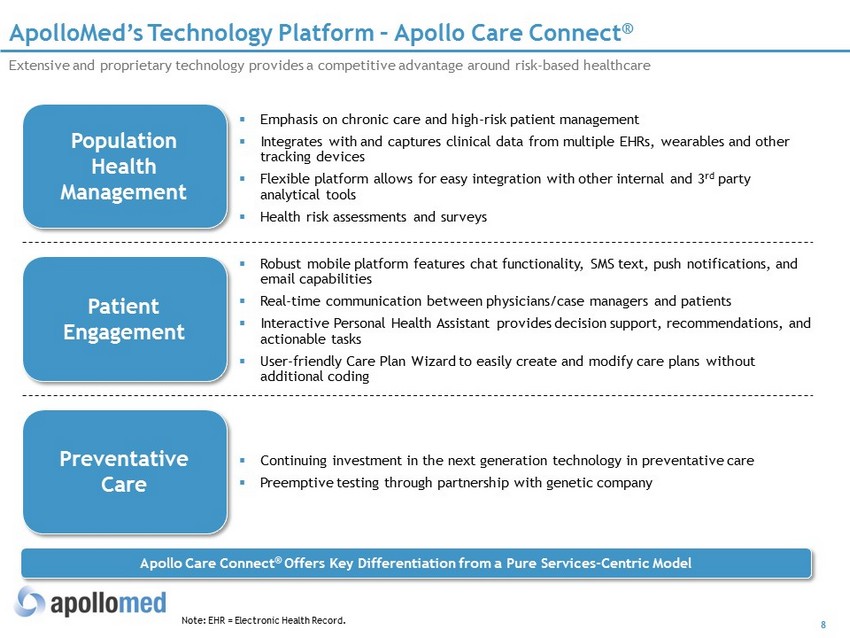

8 ApolloMed’s Technology Platform – Apollo Care Connect ® ▪ Emphasis on chronic care and high - risk patient management ▪ Integrates with and captures clinical data from multiple EHRs, wearables and other tracking devices ▪ Flexible platform allows for easy integration with other internal and 3 rd party analytical tools ▪ Health risk assessments and surveys Population Health Management Patient Engagement ▪ Continuing investment in the next generation technology in preventative care ▪ Preemptive testing through partnership with genetic company Preventative Care Extensive and proprietary technology provides a competitive advantage around risk - based healthcare Apollo Care Connect ® Offers Key Differentiation f rom a Pure Services - Centric Model ▪ Robust mobile platform features chat functionality, SMS text , push notifications , and email capabilities ▪ Real - time communication between physicians/case managers and patients ▪ Interactive Personal Health Assistant provides decision support, recommendations, and actionable tasks ▪ User - friendly Care Plan Wizard to easily create and modify care plans without additional coding Note: EHR = Electronic Health Record.

9 Apollo Care Connect ® Technology Snapshots

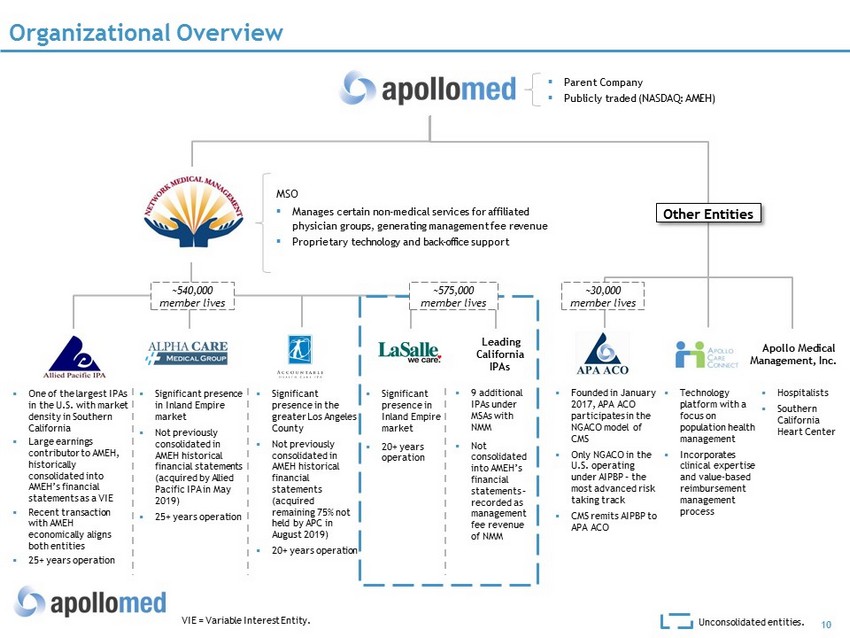

10 VIE = Variable Interest Entity. Organizational Overview Unconsolidated entities. Other Entities ▪ One of the largest IPAs in the U.S. with market density in Southern California ▪ Large earnings contributor to AMEH, historically consolidated into AMEH’s financial statements as a VIE ▪ Recent transaction with AMEH economically aligns both entities ▪ 25 + years operation ▪ Significant presence in Inland Empire market ▪ Not previously consolidated in AMEH historical financial statements ( acquired by Allied Pacific IPA in May 2019) ▪ 25+ years operation Apollo Medical Management, Inc. ▪ Parent Company ▪ Publicly traded (NASDAQ: AMEH) ▪ Founded in January 2017, APA ACO participates in the NGACO model of CMS ▪ Only NGACO in the U.S. operating under AIPBP – the most advanced risk taking track ▪ CMS remits AIPBP to APA ACO ▪ Hospitalists ▪ Southern California Heart Center MSO ▪ Manages certain non - medical services for affiliated physician groups, generating management fee revenue ▪ Proprietary technology and back - office support ▪ 9 additional IPAs under MSAs with NMM ▪ Not consolidated into AMEH’s financial statements – recorded as management fee revenue of NMM Leading California IPAs ▪ Significant presence in the greater Los Angeles County ▪ Not previously consolidated in AMEH historical financial statements (acquired remaining 75% not held by APC in August 2019) ▪ 20+ years operation ▪ Significant presence in Inland Empire market ▪ 20+ years operation ~575,000 member lives ~540,000 member lives ~30,000 member lives ▪ Technology platform with a focus on population health management ▪ Incorporates clinical expertise and value - based reimbursement management process

11 ApolloMed Key Differentiators ▪ We recognize the importance of the physician’s role in influencing and driving the value proposition in transforming healthcare Physician - driven ▪ We respect the physician’s right to remain independent and recognize there are multiple pathways and opportunities to share in creating value through lower cost and efficient care management Independence ▪ We provide technology and tools to lessen the administrative burden and allow doctors to focus on providing healthcare Reduced Administrative Burden ▪ We provide a framework for assuring the continued quality of care Quality Framework

12 ApolloMed Key Recent Accomplishments ; December 2017 Closed merger with ApolloMed and NMM ; May 2019 APC completed acquisition of Alpha Care Medical Group ; August 2019 APC completed acquisition of Accountable Healthcare IPA ; September 2019 Completed APC transaction (including $290mm credit facilities) ; October 2019 Entered into MSA with IPA serving ~145,000 new members ; November 2019 APC awarded Elite status for America’s Physician Groups Standard of Excellence Survey for 2019 Note: MSA = Master Service Agreement.

13 Experienced Management Team with a History of Success Name Title Year Joined Apollo Med Background Kenneth Sim, M.D. Executive Chairman and Co - CEO 2006 ▪ Also serves as Chairman of APC ▪ Holds bachelor’s degree from UCLA and M.D. from Loma Linda University School of Medicine and the Autonomous University of Guadalajara, Guadalajara, Mexico ▪ General surgeon Thomas S. Lam, M.D., M.P.H. Co - CEO and President 2005 ▪ Member of AMEH’s Board of Directors since 2016, CEO and CFO of APC since 2014 ▪ Also serves as CEO and board member of NMM ▪ Received medical training from New York Medical College and gastroenterology training from Georgetown University Eric Chin Chief Financial Officer 2018 ▪ Also serves as CFO of NMM, previously served as Controller / Head of Finance – Real Estate of Public Storage, AVP of Financial Reporting at Alexandria REIT and Assurance Senior Manager at E&Y ▪ 17+ years of financial experience ▪ Holds a B.A. from UCLA and is a licensed CPA Hing Ang Chief Operating Officer 2007 ▪ Previously served as Senior Director of Operations of NMM ▪ Fellow of the Association of Chartered Certified Accountants in England and a licensed CPA Adrian Vazquez, M.D. Chief Medical Officer 2001 ▪ Previously served as President and Chairman of the Board of ApolloMed prior to the NMM merger and co - founder of ApolloMed Hospitalists ▪ Holds a B.S. and M.D. from UC Irvine ▪ Internal medicine specialist Albert Young, M.D. Chief Administrative Officer 2006 ▪ Holds an M.D. from West Virginia University School of Medicine and a Master’s in Public Health from UCLA; completed internal medicine residency and Fellowship in pulmonary medicine at USC Medical Center ▪ Pulmonology specialist Brandon Sim Interim Chief Technology Officer 2019 ▪ Previously served as Quantitative Researcher at Citadel Securities and Chief Technology Officer at Theratech ▪ Holds a B.A. in Statistics and Physics and M.S. in Computer Science and Engineering from Harvard University In Addition to the Executive Management team, ApolloMed h as a Deep and Experienced Bench of Senior Managers

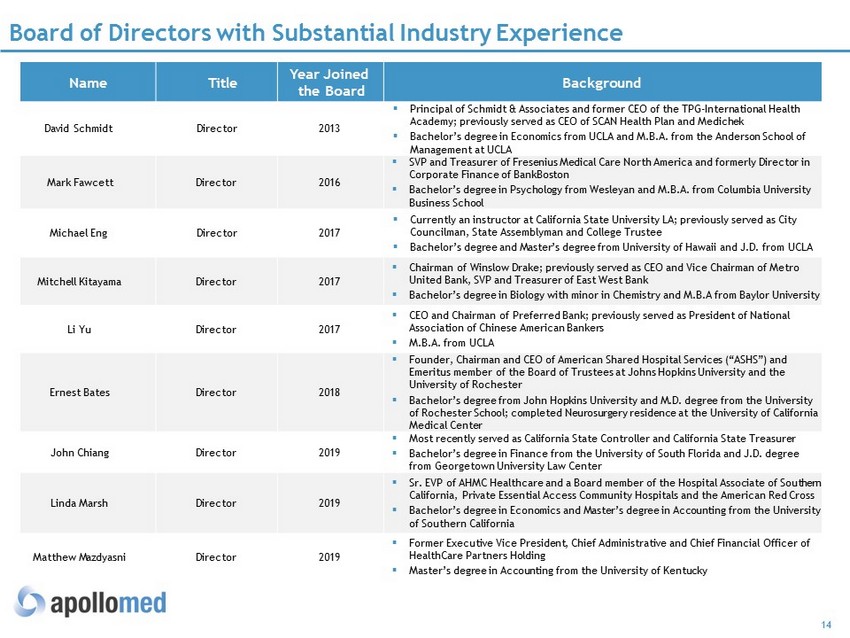

14 Board of Directors with Substantial Industry Experience Name Title Year Joined the Board Background David Schmidt Director 2013 ▪ Principal of Schmidt & Associates and former CEO of the TPG - International Health Academy; previously served as CEO of SCAN Health Plan and Medichek ▪ Bachelor’s degree in Economics from UCLA and M.B.A. from the Anderson School of Management at UCLA Mark Fawcett Director 2016 ▪ SVP and Treasurer of Fresenius Medical Care North America and formerly Director in Corporate Finance of BankBoston ▪ Bachelor’s degree in Psychology from Wesleyan and M.B.A. from Columbia University Business School Michael Eng Director 2017 ▪ Currently an instructor at California State University LA; previously served as City Councilman, State Assemblyman and College Trustee ▪ Bachelor’s degree and Master’s degree from University of Hawaii and J.D. from UCLA Mitchell Kitayama Director 2017 ▪ Chairman of Winslow Drake; previously served as CEO and Vice Chairman of Metro United Bank, SVP and Treasurer of East West Bank ▪ Bachelor’s degree in Biology with minor in Chemistry and M.B.A from Baylor University Li Yu Director 2017 ▪ CEO and Chairman of Preferred Bank; previously served as President of National Association of Chinese American Bankers ▪ M.B.A. from UCLA Ernest Bates Director 2018 ▪ Founder, Chairman and CEO of American Shared Hospital Services (“ASHS”) and Emeritus member of the Board of Trustees at Johns Hopkins University and the University of Rochester ▪ Bachelor’s degree from John Hopkins University and M.D. degree from the University of Rochester School; completed Neurosurgery residence at the University of California Medical Center John Chiang Director 2019 ▪ Most recently served as California State Controller and California State Treasurer ▪ Bachelor’s degree in Finance from the University of South Florida and J.D. degree from Georgetown University Law Center Linda Marsh Director 2019 ▪ Sr. EVP of AHMC Healthcare and a Board member of the Hospital Associate of Southern California, Private Essential Access Community Hospitals and the American Red Cross ▪ Bachelor’s degree in Economics and Master’s degree in Accounting from the University of Southern California Matthew Mazdyasni Director 2019 ▪ Former Executive Vice President, Chief Administrative and Chief Financial Officer of HealthCare Partners Holding ▪ Master’s degree in Accounting from the University of Kentucky

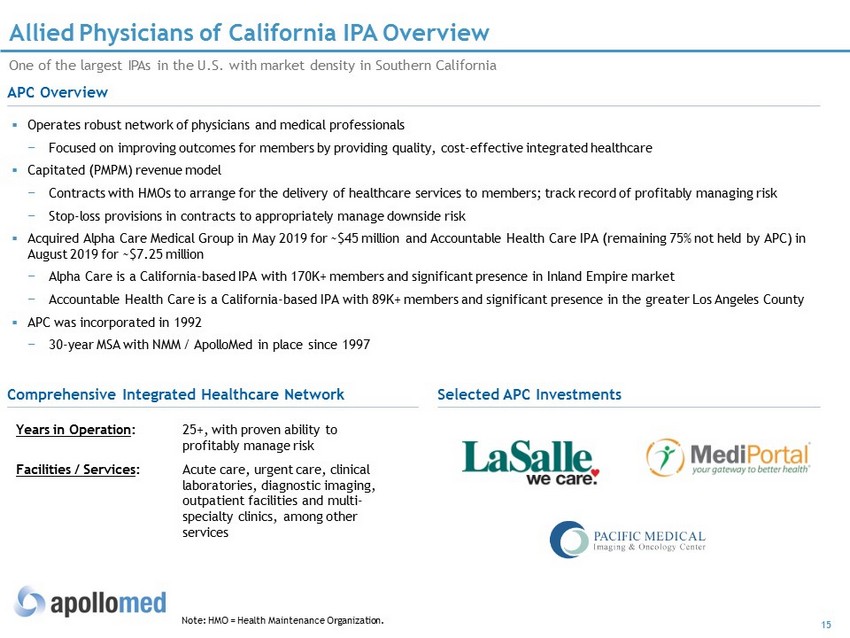

15 Allied Physicians of California IPA Overview Note: HMO = Health Maintenance Organization . One of the largest IPAs in the U.S. with market density in Southern California ▪ Operates robust network of physicians and medical professionals − Focused on improving outcomes for members by providing quality, cost - effective integrated healthcare ▪ Capitated (PMPM) revenue model − Contracts with HMOs to arrange for the delivery of healthcare services to members; track record of profitably managing risk − Stop - loss provisions in contracts to appropriately manage downside risk ▪ Acquired Alpha Care Medical Group in May 2019 for ~$45 million and Accountable Health Care IPA (remaining 75% not held by APC) in August 2019 for ~$ 7.25 million − Alpha Care is a California - based IPA with 170K+ members and significant presence in Inland Empire market − Accountable Health Care is a California - based IPA with 89K + members and significant presence in the greater Los Angeles County ▪ APC was incorporated in 1992 − 30 - year MSA with NMM / ApolloMed in place since 1997 Years in Operation : 25+, with proven ability to profitably manage risk Facilities / Services : Acute care, urgent care, clinical laboratories, diagnostic imaging, outpatient facilities and multi - specialty clinics, among other services Selected APC Investments APC Overview Comprehensive Integrated Healthcare Network

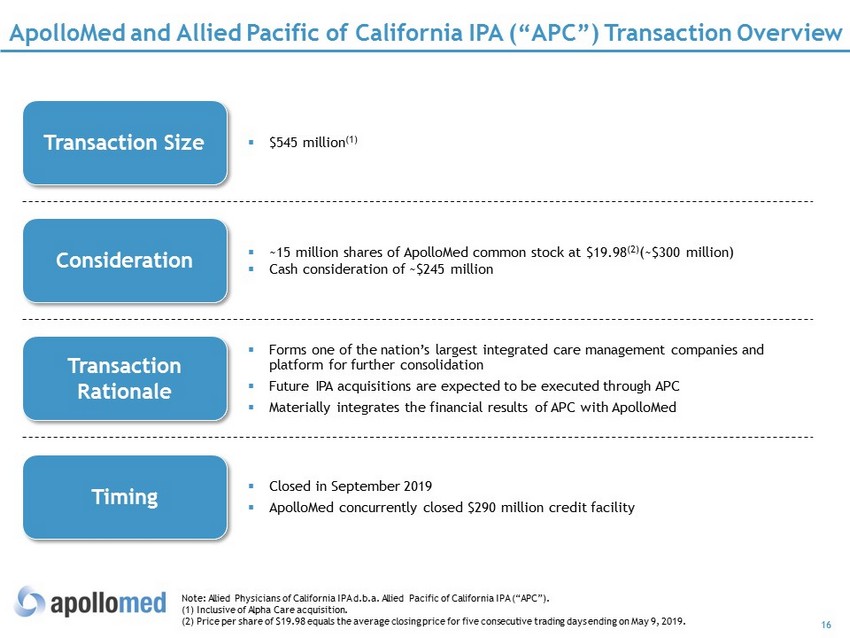

16 ApolloMed and Allied Pacific of California IPA (“APC”) Transaction Overview ▪ $545 million (1) Transaction Size ▪ ~15 million shares of ApolloMed common stock at $19.98 (2) (~$300 million) ▪ Cash consideration of ~$245 million Consideration ▪ Forms one of the nation’s largest integrated care management companies and platform for further consolidation ▪ Future IPA acquisitions are expected to be executed through APC ▪ Materially integrates the financial results of APC with ApolloMed Transaction Rationale ▪ Closed in September 2019 ▪ ApolloMed concurrently closed $290 million credit facility Timing Note: Allied Physicians of California IPA d.b.a. Allied Pacific of California IPA (“APC”). (1) Inclusive of Alpha Care acquisition. (2) Price per share of $19.98 equals the average closing price for five consecutive trading days ending on May 9, 2019.

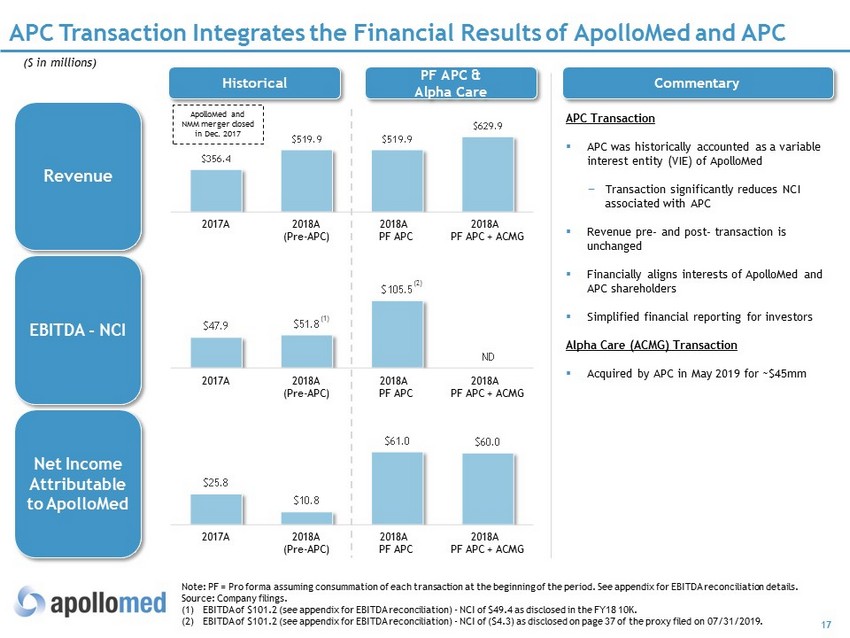

17 $356.4 $519.9 $519.9 $629.9 $47.9 $51.8 $105.5 ND APC Transaction Integrates the Financial Results of ApolloMed and APC Note: PF = Pro forma assuming consummation of each transaction at the beginning of the period. See appendix for EBITDA reconc ili ation details. Source: Company filings. (1) EBITDA of $101.2 (see appendix for EBITDA reconciliation) - NCI of $49.4 as disclosed in the FY18 10K. (2) EBITDA of $101.2 (see appendix for EBITDA reconciliation ) - NCI of ($4.3) as disclosed on page 37 of the proxy filed on 07/31/2019. APC Transaction ▪ APC was historically accounted as a variable interest entity (VIE) of ApolloMed − Transaction significantly reduces NCI associated with APC ▪ Revenue pre - and post - transaction is unchanged ▪ Financially aligns interests of ApolloMed and APC shareholders ▪ Simplified financial reporting for investors Alpha Care (ACMG) Transaction ▪ Acquired by APC in May 2019 for ~$45mm EBITDA - NCI Net Income Attributable to ApolloMed ($ in millions) Revenue PF APC & Alpha Care Historical 2018A (Pre - APC) 2017A 2018A PF APC 2018A PF APC + ACMG $25.8 $10.8 $61.0 $60.0 2018A (Pre - APC) 2017A 2018A PF APC 2018A PF APC + ACMG Commentary 2018A (Pre - APC) 2017A 2018A PF APC 2018A PF APC + ACMG ApolloMed and NMM merger closed in Dec. 2017 (1) (2)

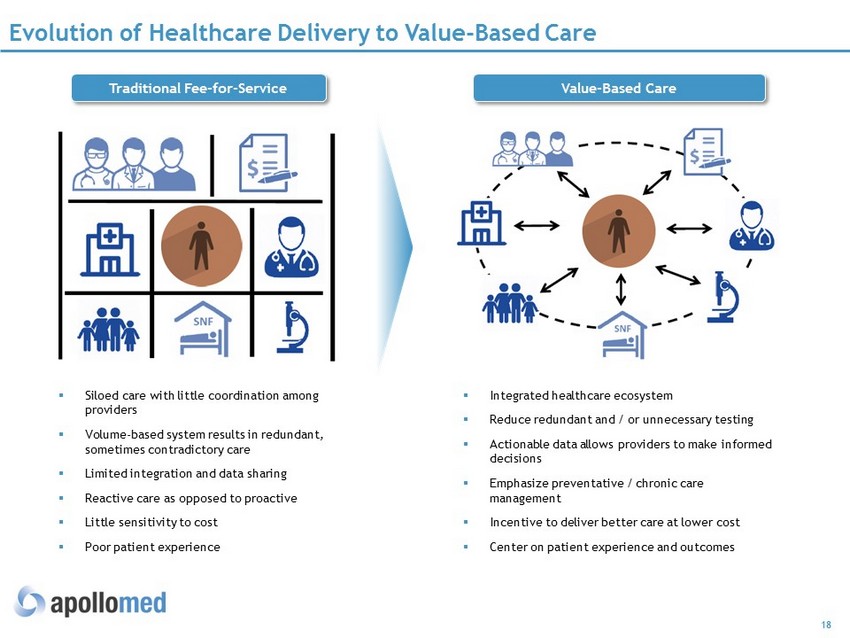

18 Evolution of Healthcare Delivery to Value - Based Care ▪ Siloed care with little coordination among providers ▪ Volume - based system results in redundant, sometimes contradictory care ▪ Limited integration and data sharing ▪ Reactive care as opposed to proactive ▪ Little sensitivity to cost ▪ Poor patient experience ▪ Integrated healthcare ecosystem ▪ Reduce redundant and / or unnecessary testing ▪ Actionable data allows providers to make informed decisions ▪ Emphasize preventative / chronic care management ▪ Incentive to deliver better care at lower cost ▪ Center on patient experience and outcomes Traditional Fee - for - Service Value - Based Care

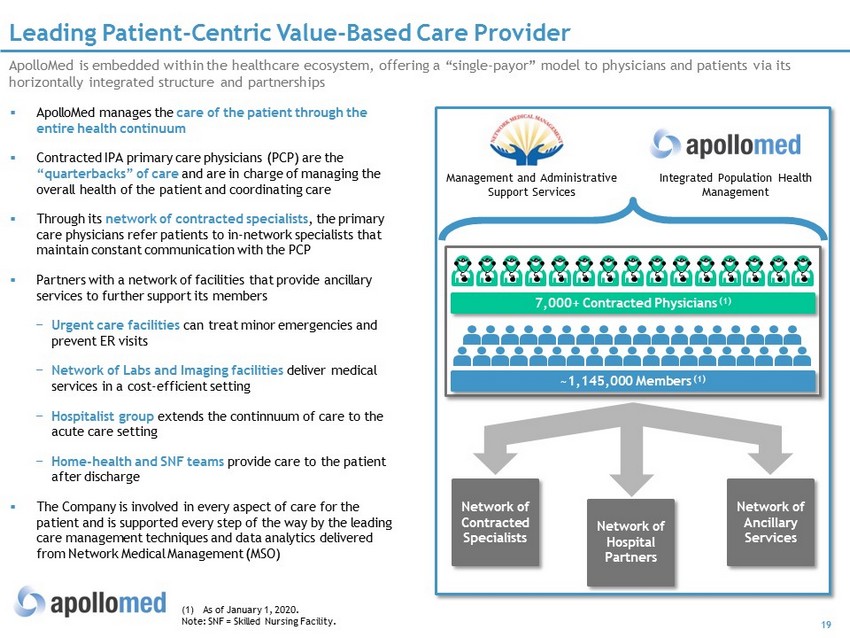

19 Leading Patient - Centric Value - Based Care Provider (1) As of January 1, 2020. Note: SNF = Skilled Nursing Facility. ApolloMed is embedded within the healthcare ecosystem, offering a “ single - payor ” model to physicians and patients via its horizontally integrated structure and partnerships ▪ ApolloMed manages the care of the patient through the entire health continuum ▪ Contracted IPA primary care physicians (PCP) are the “quarterbacks” of care and are in charge of managing the overall health of the patient and coordinating care ▪ Through its network of contracted specialists , the primary care physicians refer patients to in - network specialists that maintain constant communication with the PCP ▪ Partners with a network of facilities that provide ancillary services to further support its members − Urgent care facilities can treat minor emergencies and prevent ER visits − Network of Labs and Imaging facilities deliver medical services in a cost - efficient setting − Hospitalist group extends the continnuum of care to the acute care setting − Home - health and SNF teams provide care to the patient after discharge ▪ The Company is involved in every aspect of care for the patient and is supported every step of the way by the leading care management techniques and data analytics delivered from Network Medical Management (MSO) Network of Contracted Specialists Network of Hospital Partners Network of Ancillary Services 7 ,000+ Contracted Physicians (1) ~1,145,000 Members (1) Management and Administrative Support Services Integrated Population Health Management

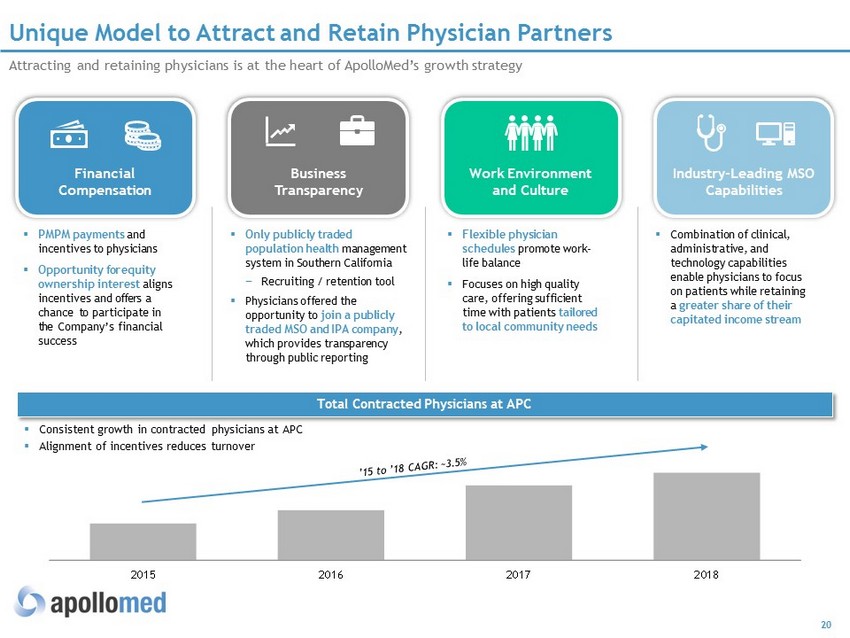

20 2015 2016 2017 2018 ▪ Combination of clinical, administrative, and technology capabilities enable physicians to focus on patients while retaining a greater share of their capitated income stream ▪ Flexible physician schedules promote work - life balance ▪ Focuses on high quality care, offering sufficient time with patients tailored to local community needs Unique Model to Attract and Retain Physician Partners Attracting and retaining physicians is at the heart of ApolloMed’s growth strategy Business Transparency Financial Compensation Work Environment and Culture Industry - Leading MSO Capabilities ▪ PMPM payments and incentives to physicians ▪ Opportunity for equity ownership interest aligns incentives and offers a chance to participate in the Company’s financial success Total Contracted Physicians at APC ▪ Only publicly traded population health management system in Southern California − Recruiting / retention tool ▪ Physicians offered the opportunity to join a publicly traded MSO and IPA company , which provides transparency through public reporting ▪ Consistent growth in contracted physicians at APC ▪ Alignment of incentives reduces turnover

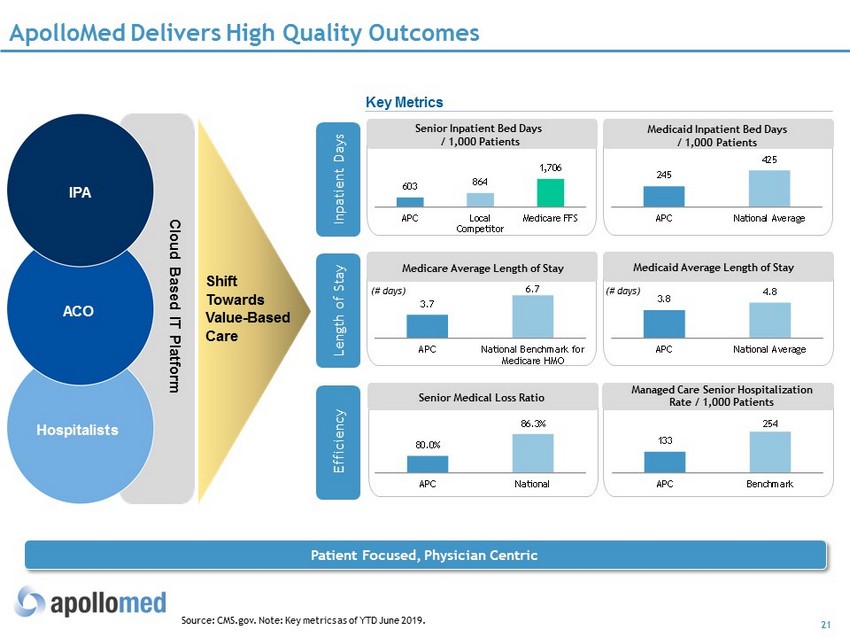

21 Medicare Average Length of Stay ApolloMed Delivers High Quality Outcomes Cloud Based IT Platform Hospitalists A CO IPA Shift T owards Value - Based Care Key Metrics Senior Inpatient Bed Days / 1,000 Patients 603 864 1,706 APC Local Competitor Medicare FFS * Senior Medical Loss Ratio 3.7 6.7 APC National Benchmark for Medicare HMO 245 425 APC National Average Medicaid Inpatient Bed Days / 1,000 Patients 133 254 APC Benchmark (# days) (# days) Source: CMS.gov. Note: Key metrics as of YTD June 2019. Managed Care Senior Hospitalization Rate / 1,000 Patients Medicaid Average Length of Stay Inpatient Days Length of Stay Efficiency Patient Focused, Physician Centric 3.8 4.8 APC National Average 80.0% 86.3% APC National

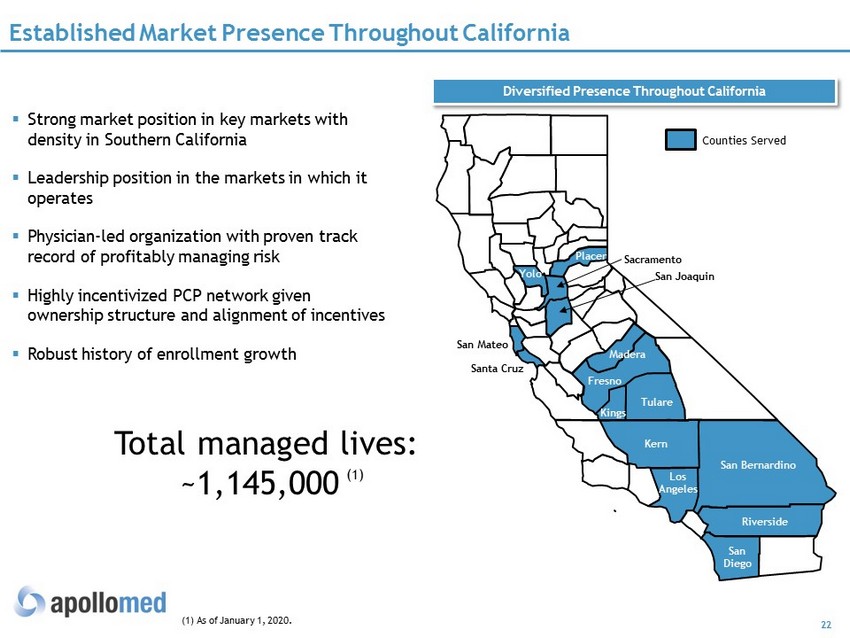

22 San Bernardino Riverside San Diego Los Angeles Kern Tulare Kings Fresno Madera Santa Cruz San Mateo Yolo Placer Sacramento San Joaquin Established Market Presence Throughout California Diversified Presence Throughout California Counties Served ▪ Strong market position in key markets with density in Southern California ▪ Leadership position in the markets in which it operates ▪ Physician - led organization with proven track record of profitably managing risk ▪ Highly incentivized PCP network given ownership structure and alignment of incentives ▪ Robust history of enrollment growth Total managed lives: ~1,145,000 (1) (1) As of January 1, 2020.

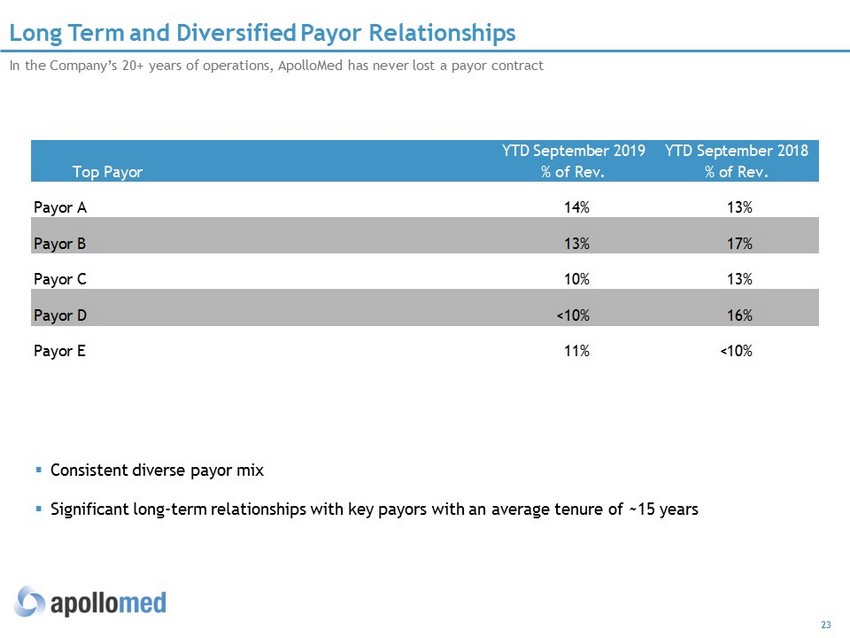

23 Long Term and Diversified Payor Relationships Top Payor YTD September 2019 % of Rev. YTD September 2018 % of Rev. Payor A 14% 13% Payor B 13% 17% Payor C 10% 13% Payor D <10% 16% Payor E 11% <10% In the Company’s 20+ years of operations, ApolloMed has never lost a payor contract ▪ Consistent diverse payor mix ▪ Significant long - term relationships with key payors with an average tenure of ~15 years

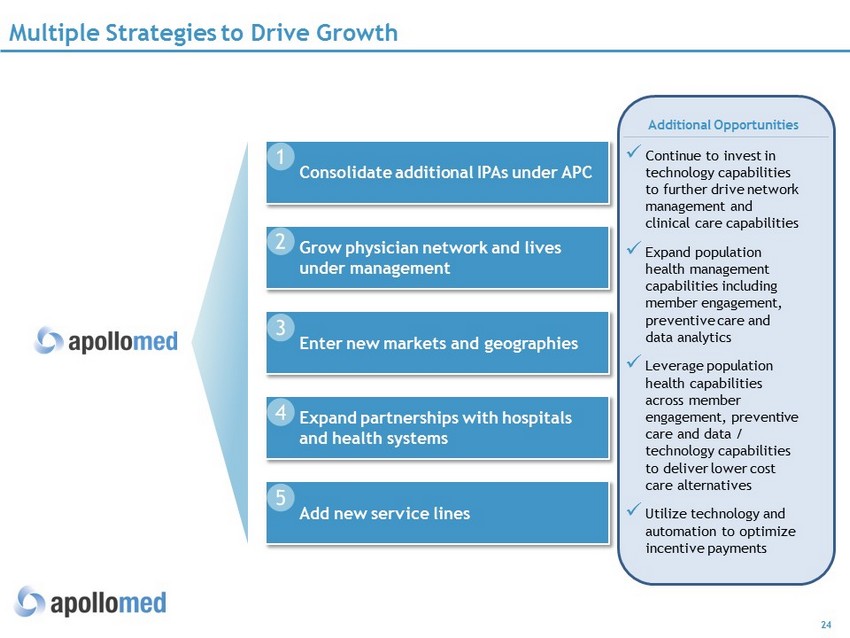

24 Multiple Strategies to Drive Growth x Continue to invest in technology capabilities to further drive network management and clinical care capabilities x Expand population health management capabilities including member engagement, preventive care and data analytics x Leverage population health capabilities across member engagement, preventive care and data / technology capabilities to deliver lower cost care alternatives x Utilize technology and automation to optimize incentive payments Additional Opportunities Grow physician network and lives under management Enter new markets and geographies Expand partnerships with hospitals and health systems Add new service lines Consolidate additional IPAs under APC

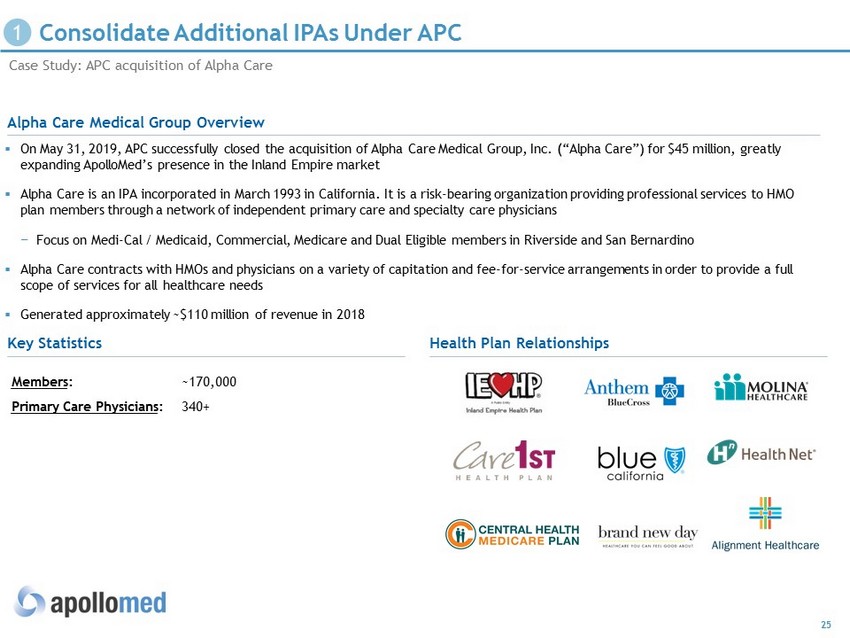

25 Case Study: APC acquisition of Alpha Care ▪ On May 31, 2019, APC successfully closed the acquisition of Alpha Care Medical Group, Inc. (“Alpha Care”) for $45 million, gr eat ly expanding ApolloMed’s presence in the Inland Empire market ▪ Alpha Care is an IPA incorporated in March 1993 in California. It is a risk - bearing organization providing professional services to HMO plan members through a network of independent primary care and specialty care physicians − Focus on Medi - Cal / Medicaid, Commercial, Medicare and Dual Eligible members in Riverside and San Bernardino ▪ Alpha Care contracts with HMOs and physicians on a variety of capitation and fee - for - service arrangements in order to provide a full scope of services for all healthcare needs ▪ Generated approximately ~$110 million of revenue in 2018 Members : ~170,000 Primary Care Physicians : 340+ Alpha Care Medical Group Overview Key Statistics Health Plan Relationships Consolidate Additional IPAs Under APC

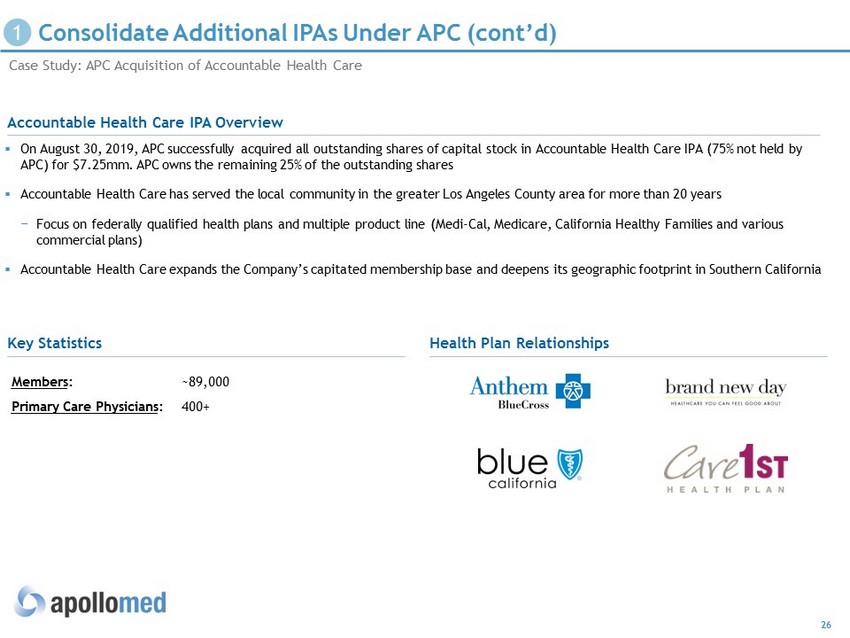

26 Consolidate Additional IPAs U nder APC (cont’d) Case Study: APC Acquisition of Accountable Health Care ▪ On August 30, 2019, APC successfully acquired all outstanding shares of capital stock in Accountable Health Care IPA (75% not he ld by APC) for $7.25mm. APC owns the remaining 25% of the outstanding shares ▪ Accountable Health Care has served the local community in the greater Los Angeles County area for more than 20 years − Focus on federally qualified health plans and multiple product line (Medi - Cal, Medicare, California Healthy Families and various commercial plans) ▪ Accountable Health Care expands the Company’s capitated membership base and deepens its geographic footprint in Southern Cali for nia Members : ~89,000 Primary Care Physicians : 400+ Accountable Health Care IPA Overview Key Statistics Health Plan Relationships

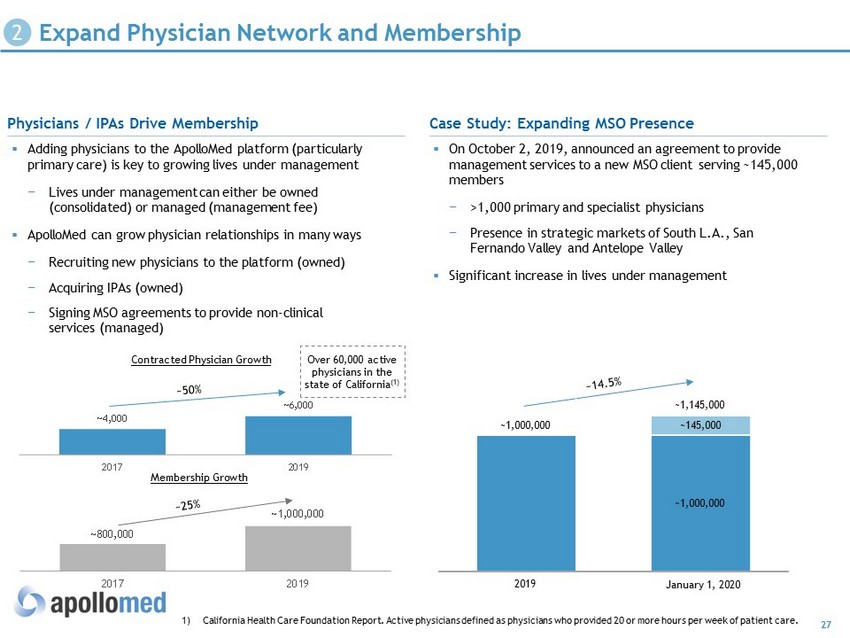

27 ▪ Adding physicians to the ApolloMed platform (particularly primary care) is key to growing lives under management − Lives under management can either be owned (consolidated) or managed (management fee) ▪ ApolloMed can grow physician relationships in many ways − Recruiting new physicians to the platform (owned) − Acquiring IPAs (owned) − Signing MSO agreements to provide non - clinical services (managed) 1) California Health Care Foundation Report. Active physicians defined as physicians who provided 20 or more hours per week of p ati ent care. ▪ On October 2, 2019, announced an agreement to provide management services to a new MSO client serving ~145,000 members − >1,000 primary and specialist physicians − Presence in strategic markets of South L.A., San Fernando Valley and Antelope Valley ▪ Significant increase in lives under management Expand Physician Network and Membership Physicians / IPAs Drive Membership Case Study: Expanding MSO Presence ~800,000 ~1,000,000 2017 2019 ~4,000 ~6,000 2017 2019 Contracted Physician Growth Membership Growth Over 60,000 active physicians in the state of California (1) ~1,000,000 ~1,000,000 ~145,000 ~1,145,000 2019 January 1, 2020

28 Multi - Faceted Growth Opportunity Add New Service Lines Expand Partnerships Enter New Markets and Geographies ▪ Consistent dialogue with new IPAs to expand into new markets ▪ Recent expansion into San Bernardino, San Mateo, Riverside and Orange counties ▪ Will be selective and opportunistic in expanding outside of California market ▪ Enter brick and mortar medical space through physician practice management ▪ Mid - level nurse practitioners / temporary staffing services ▪ Continues to invest in next generation technology, preventative care and automation to further drive clinical care capabilities ▪ Actively looking for additional partnerships to expand footprint

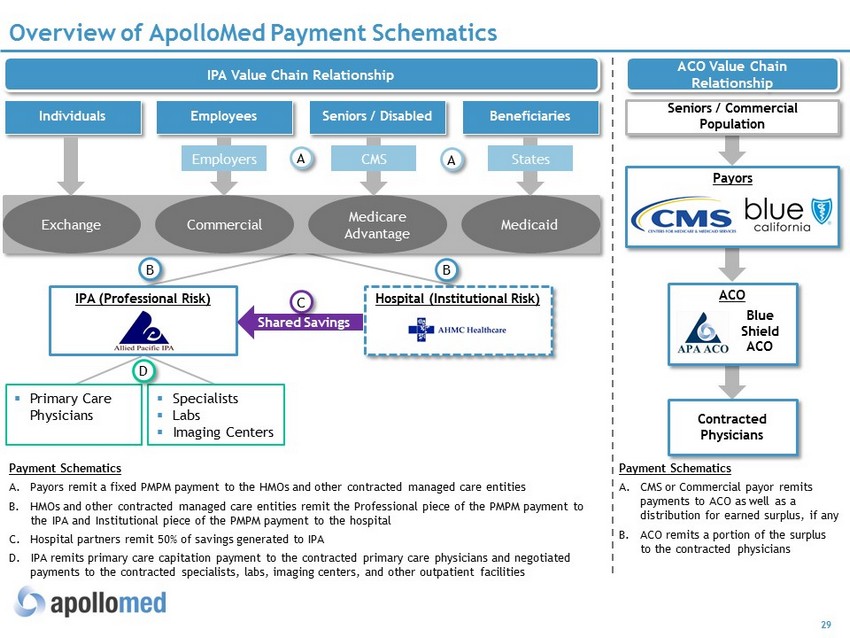

29 Payors Overview of ApolloMed Payment Schematics IPA Value Chain Relationship ACO Value Chain Relationship Individuals Employees Seniors / Disabled Beneficiaries Exchange Commercial Medicare Advantage Medicaid Employers CMS States IPA (Professional Risk) Hospital ( Institutional Risk) Shared Savings ▪ Primary Care Physicians Seniors / Commercial Population Payment Schematics A. Payors remit a fixed PMPM payment to the HMOs and other contracted managed care entities B. HMOs and other contracted managed care entities remit the Professional piece of the PMPM payment to the IPA and Institutional piece of the PMPM payment to the hospital C. Hospital partners remit 50% of savings generated to IPA D. IPA remits primary care capitation payment to the contracted primary care physicians and negotiated payments to the contracted specialists, labs, imaging centers, and other outpatient facilities ACO Contracted Physicians Payment Schematics A. CMS or Commercial payor remits payments to ACO as well as a distribution for earned surplus, if any B. ACO remits a portion of the surplus to the contracted physicians ▪ Specialists ▪ Labs ▪ Imaging Centers A A B B D C Blue Shield ACO

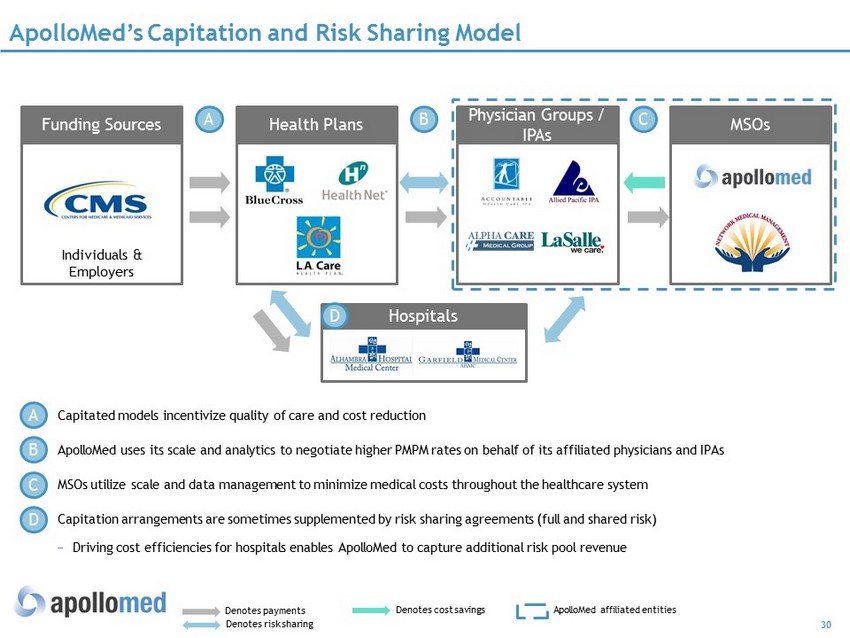

30 ApolloMed’s Capitation and Risk Sharing Model Individuals & Employers Funding Sources Health Plans Physician Groups / IPAs MSOs Denotes payments Denotes risk sharing Denotes cost savings Hospitals ▪ Capitated models incentivize quality of care and cost reduction ▪ ApolloMed uses its scale and analytics to negotiate higher PMPM rates on behalf of its affiliated physicians and IPAs ▪ MSOs utilize scale and data management to minimize medical costs throughout the healthcare system ▪ Capitation arrangements are sometimes supplemented by risk sharing agreements (full and shared risk) − Driving cost efficiencies for hospitals enables ApolloMed to capture additional risk pool revenue A B C D A B C D ApolloMed affiliated entities

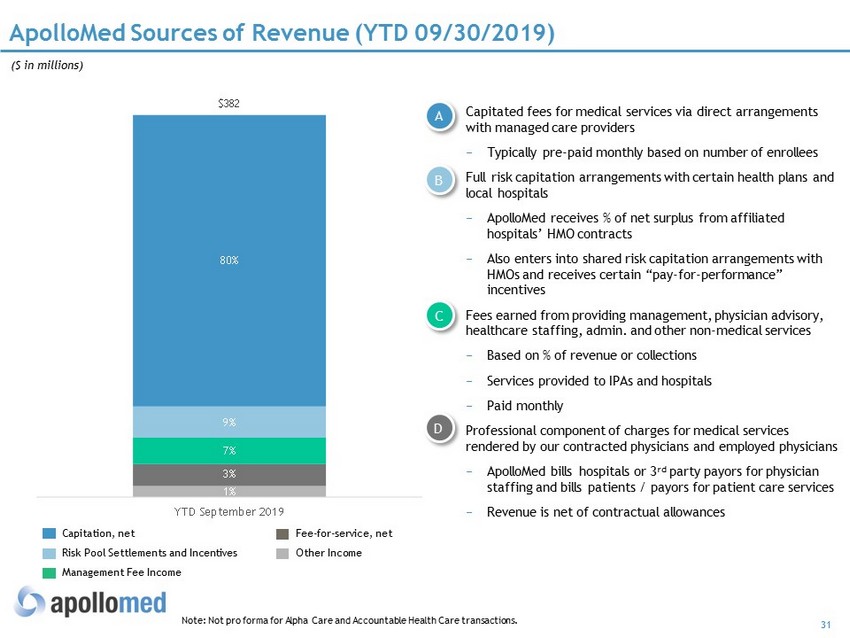

31 1% 3% 7% 9% 80% $382 YTD September 2019 Note: Not pro forma for Alpha Care and Accountable Health Care transactions. ApolloMed Sources of Revenue (YTD 09/30/2019) − Capitated fees for medical services via direct arrangements with managed care providers − Typically pre - paid monthly based on number of enrollees − Full risk capitation arrangements with certain health plans and local hospitals − ApolloMed receives % of net surplus from affiliated hospitals’ HMO contracts − Also enters into shared risk capitation arrangements with HMOs and receives certain “pay - for - performance” incentives − Fees earned from providing management, physician advisory, healthcare staffing, admin. and other non - medical services − Based on % of revenue or collections − Services provided to IPAs and hospitals − Paid monthly − Professional component of charges for medical services rendered by our contracted physicians and employed physicians − ApolloMed bills hospitals or 3 rd party payors for physician staffing and bills patients / payors for patient care services − Revenue is net of contractual allowances A B C D ($ in millions) Capitation, net Risk Pool Settlements and Incentives Management Fee Income Fee - for - service, net Other Income

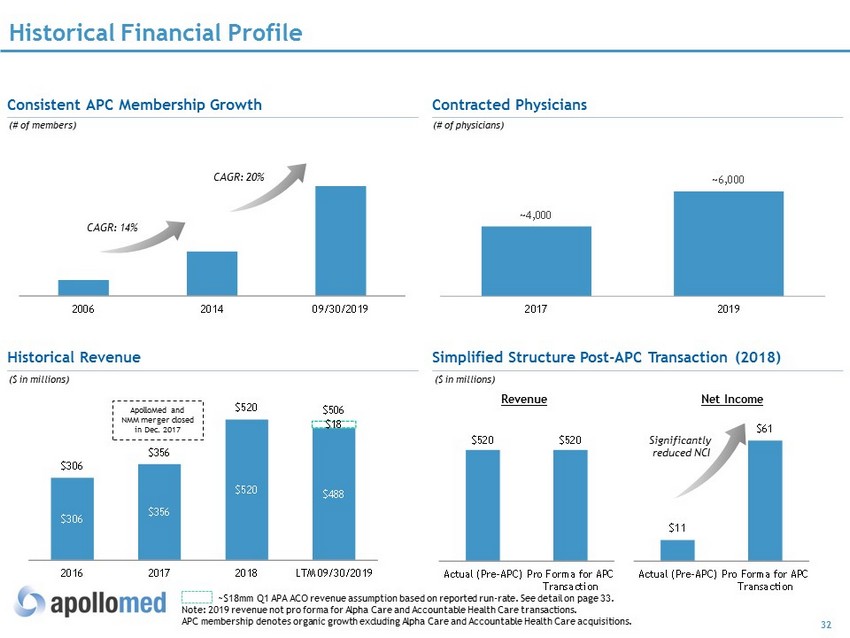

32 ~$18mm Q1 APA ACO revenue assumption based on reported run - rate. See detail on page 33. Note: 2019 revenue not pro forma for Alpha Care and Accountable Health Care transactions. APC membership denotes organic growth excluding Alpha Care and Accountable Health Care acquisitions. 2006 2014 09/30/2019 Historical Financial Profile Simplified Structure Post - APC Transaction (2018) Historical Revenue Consistent APC Membership Growth Contracted Physicians $306 $356 $520 $488 $18 $306 $356 $520 $506 2016 2017 2018 LTM 09/30/2019 $11 $61 Actual (Pre-APC) Pro Forma for APC Transaction $520 $520 Actual (Pre-APC) Pro Forma for APC Transaction Significantly reduced NCI Revenue Net Income CAGR: 14% CAGR: 20% ApolloMed and NMM merger closed in Dec. 2017 (# of members) ($ in millions) ($ in millions) ~4,000 ~6,000 2017 2019 (# of physicians)

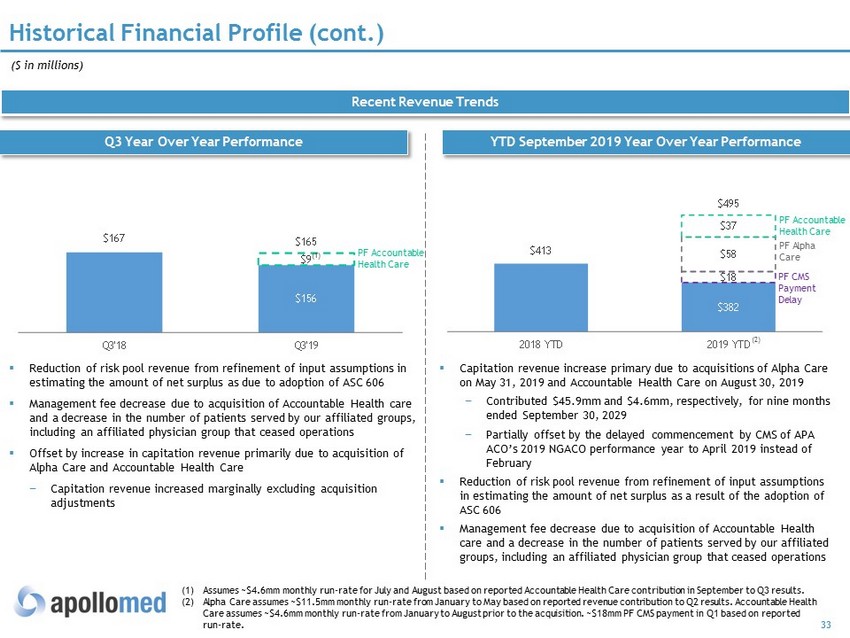

33 $413 $382 $18 $58 $37 $495 2018 YTD 2019 YTD $167 $156 $9 $165 Q3'18 Q3'19 Historical Financial Profile (cont.) ($ in millions) Recent Revenue Trends Q3 Year Over Year Performance YTD September 2019 Year Over Year Performance ▪ Reduction of risk pool revenue from refinement of input assumptions in estimating the amount of net surplus as due to adoption of ASC 606 ▪ Management fee decrease due to acquisition of Accountable Health care and a decrease in the number of patients served by our affiliated groups, including an affiliated physician group that ceased operations ▪ Offset by increase in capitation revenue primarily due to acquisition of Alpha Care and Accountable Health Care − Capitation revenue increased marginally excluding acquisition adjustments ▪ Capitation revenue increase primary due to acquisitions of Alpha Care on May 31, 2019 and Accountable Health Care on August 30, 2019 − Contributed $45.9mm and $4.6mm, respectively, for nine months ended September 30, 2029 − Partially offset by the delayed commencement by CMS of APA ACO’s 2019 NGACO performance year to April 2019 instead of February ▪ Reduction of risk pool revenue from refinement of input assumptions in estimating the amount of net surplus as a result of the adoption of ASC 606 ▪ Management fee decrease due to acquisition of Accountable Health care and a decrease in the number of patients served by our affiliated groups, including an affiliated physician group that ceased operations (1) Assumes ~$4.6mm monthly run - rate for July and August based on reported Accountable Health Care contribution in September to Q3 r esults. (2) Alpha Care assumes ~$11.5mm monthly run - rate from January to May based on reported revenue contribution to Q2 results. Accountab le Health Care assumes ~$4.6mm monthly run - rate from January to August prior to the acquisition. ~$18mm PF CMS payment in Q1 based on reported run - rate. PF CMS Payment Delay PF Alpha Care (2) (1) PF Accountable Health Care PF Accountable Health Care

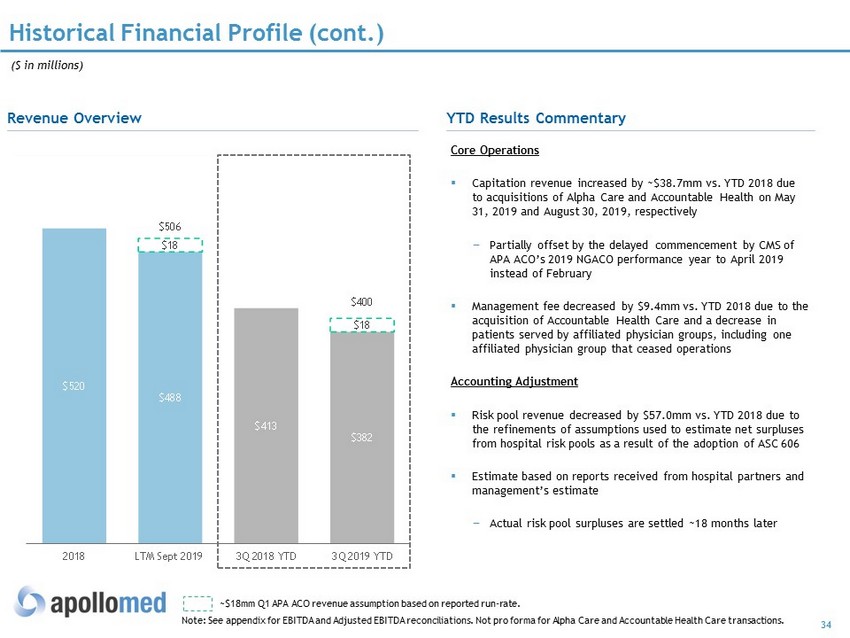

34 Historical Financial Profile (cont.) Note: See appendix for EBITDA and Adjusted EBITDA reconciliations. Not pro forma for Alpha Care and Accountable Health Care transactions. Revenue Overview YTD Results Commentary $520 $488 $413 $382 $18 $18 $506 $400 2018 LTM Sept 2019 3Q 2018 YTD 3Q 2019 YTD Core Operations ▪ Capitation revenue increased by ~$38.7mm vs. YTD 2018 due to acquisitions of Alpha Care and Accountable Health on May 31, 2019 and August 30, 2019, respectively − Partially offset by the delayed commencement by CMS of APA ACO’s 2019 NGACO performance year to April 2019 instead of February ▪ Management fee decreased by $9.4mm vs. YTD 2018 due to the acquisition of Accountable Health Care and a decrease in patients served by affiliated physician groups, including one affiliated physician group that ceased operations Accounting Adjustment ▪ Risk pool revenue decreased by $57.0mm vs. YTD 2018 due to the refinements of assumptions used to estimate net surpluses from hospital risk pools as a result of the adoption of ASC 606 ▪ Estimate based on reports received from hospital partners and management’s estimate − Actual risk pool surpluses are settled ~18 months later ($ in millions) ~$18mm Q1 APA ACO revenue assumption based on reported run - rate.

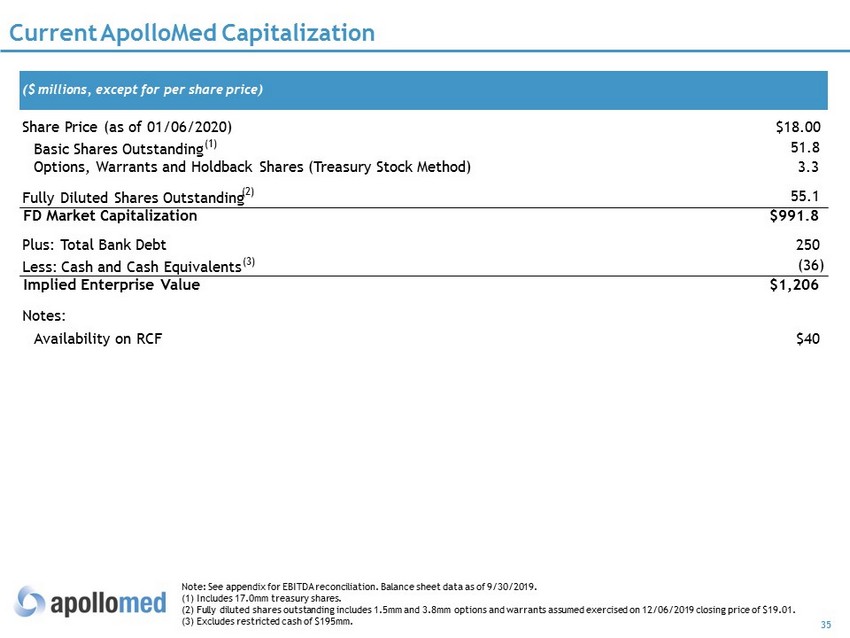

35 Current ApolloMed Capitalization Note: See appendix for EBITDA reconciliation. Balance sheet data as of 9/30/2019. (1) Includes 17.0mm treasury shares. (2) Fully diluted shares outstanding includes 1.5mm and 3.8mm options and warrants assumed exercised on 12/06/2019 closing pr ice of $19.01. (3) Excludes restricted cash of $195mm. ($ millions, except for per share price) Share Price (as of 01/06/2020) $18.00 Basic Shares Outstanding (1) 51.8 Options, Warrants and Holdback Shares (Treasury Stock Method) 3.3 Fully Diluted Shares Outstanding (2) 55.1 FD Market Capitalization $991.8 Plus: Total Bank Debt 250 Less: Cash and Cash Equivalents (3) (36) Implied Enterprise Value $1,206 Notes: Availability on RCF $40

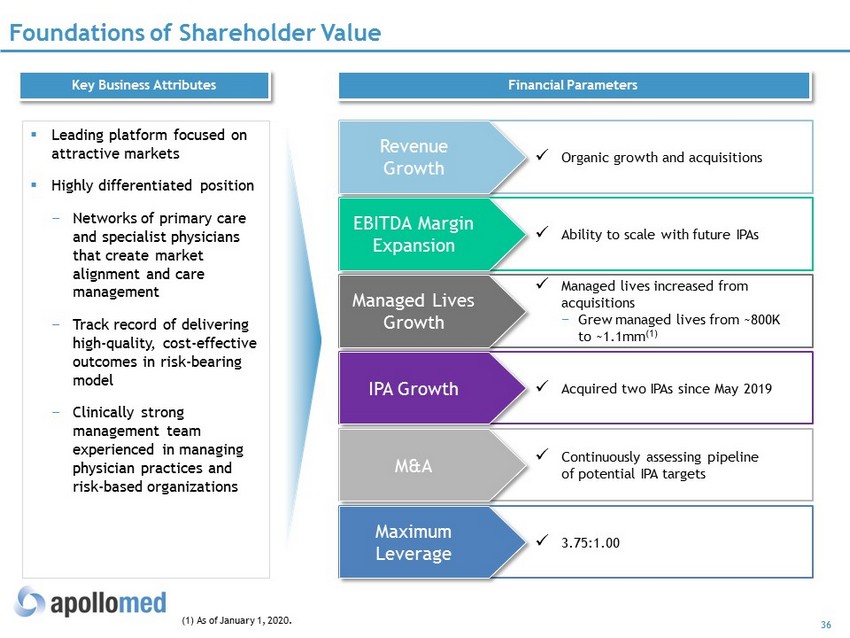

36 Foundations of Shareholder Value Financial Parameters Key Business Attributes x Organic growth and acquisitions Revenue Growth x Ability to scale with future IPAs EBITDA Margin Expansion x Managed lives increased from acquisitions − Grew managed lives from ~800K to ~1.1mm (1) Managed Lives Growth x Acquired two IPAs since May 2019 IPA Growth x 3.75:1.00 Maximum Leverage ▪ Leading platform focused on attractive markets ▪ Highly differentiated position − Networks of primary care and specialist physicians that create market alignment and care management − Track record of delivering high - quality, cost - effective outcomes in risk - bearing model − Clinically strong management team experienced in managing physician practices and risk - based organizations x Continuously assessing pipeline of potential IPA targets M&A (1) As of January 1, 2020.

Appendix

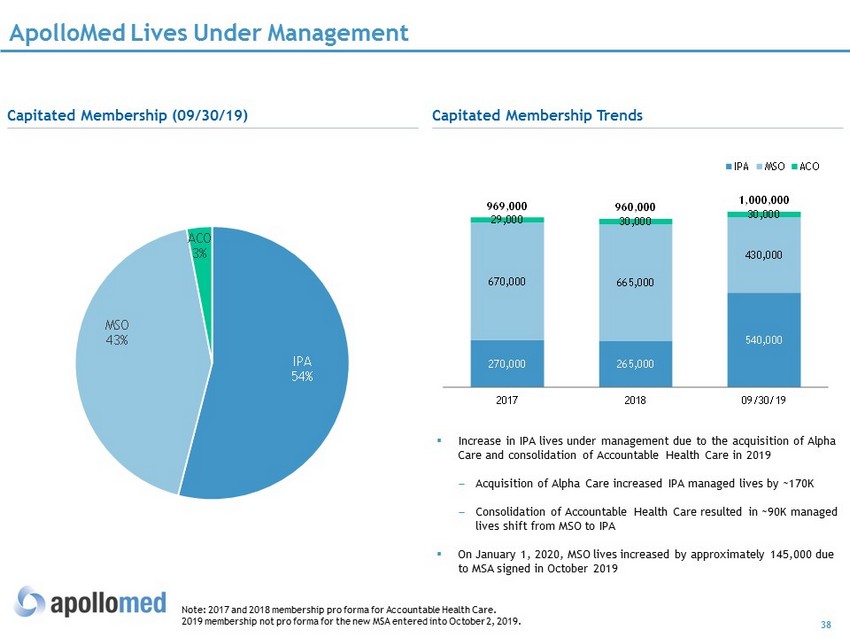

38 ApolloMed Lives Under Management Note: 2017 and 2018 membership pro forma for Accountable Health Care. 2019 membership not pro forma for the new MSA entered into October 2 , 2019 . Capitated Membership (09/30/19) Capitated Membership Trends ▪ Increase in IPA lives under management due to the acquisition of Alpha Care and consolidation of Accountable Health Care in 2019 ; Acquisition of Alpha Care increased IPA managed lives by ~170K ; Consolidation of Accountable Health Care resulted in ~90K managed lives shift from MSO to IPA ▪ On January 1, 2020, MSO lives increased by approximately 145,000 due to MSA signed in October 2019 IPA 54% MSO 43% ACO 3% 270,000 265,000 540,000 670,000 665,000 430,000 29,000 30,000 30,000 969,000 960,000 1,000,000 2017 2018 09/30/19 IPA MSO ACO

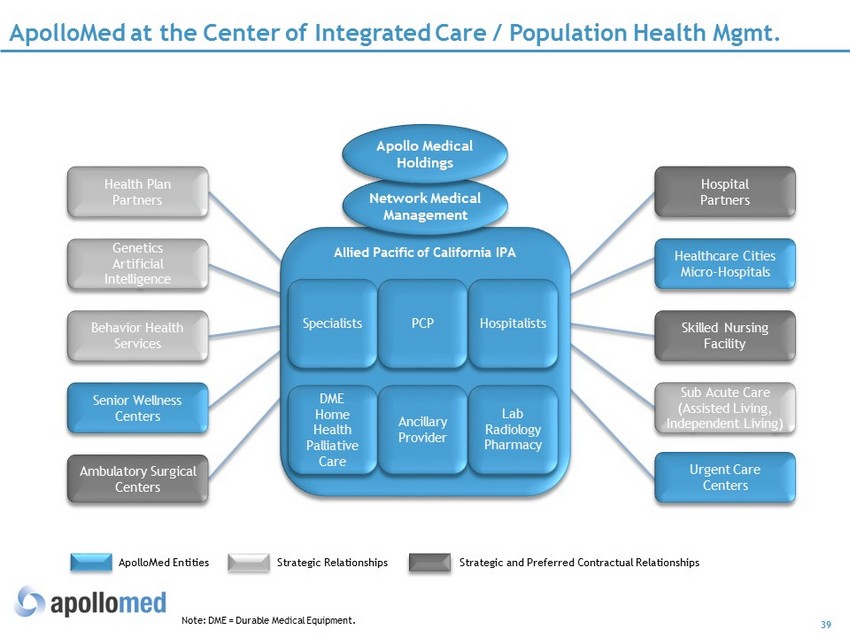

39 ApolloMed at the Center of Integrated Care / Population Health Mgmt. Health Plan Partners Genetics Artificial Intelligence Behavior Health Services Senior Wellness Centers Ambulatory Surgical Centers Hospital Partners Healthcare Cities Micro - Hospitals Skilled Nursing Facility Sub Acute Care (Assisted Living, Independent Living) Allied Pacific of California IPA Specialists PCP Hospitalists DME Home Health Palliative Care Ancillary Provider Lab Radiology Pharmacy Network Medical Management Apollo Medical Holdings ApolloMed Entities Strategic Relationships Strategic and Preferred Contractual Relationships Urgent Care Centers Note: DME = Durable Medical Equipment.

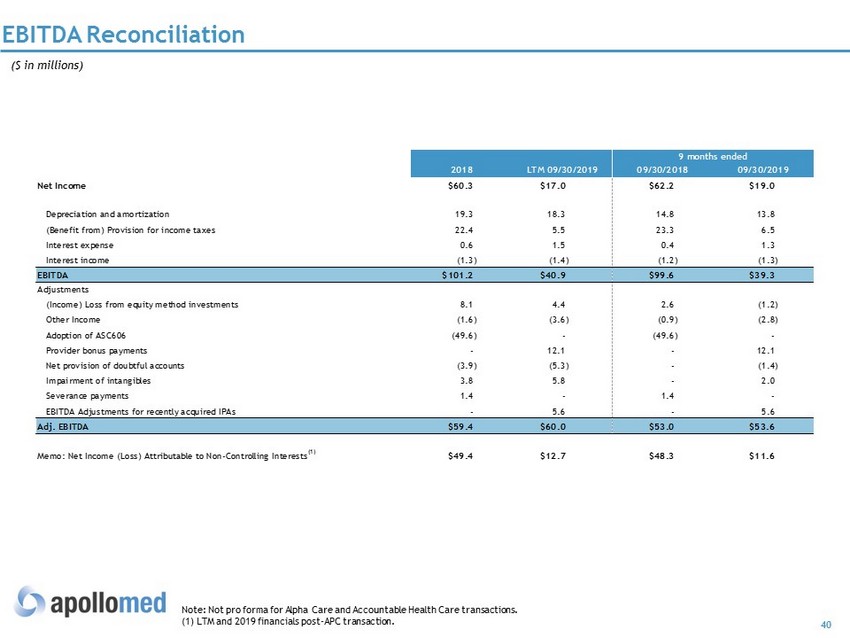

40 EBITDA Reconciliation ($ in millions) Note: Not pro forma for Alpha Care and Accountable Health Care transactions. (1) LTM and 2019 financials post - APC transaction. 9 months ended 2018 LTM 09/30/2019 09/30/2018 09/30/2019 Net Income $60.3 $17.0 $62.2 $19.0 Depreciation and amortization 19.3 18.3 14.8 13.8 (Benefit from) Provision for income taxes 22.4 5.5 23.3 6.5 Interest expense 0.6 1.5 0.4 1.3 Interest income (1.3) (1.4) (1.2) (1.3) EBITDA $101.2 $40.9 $99.6 $39.3 Adjustments (Income) Loss from equity method investments 8.1 4.4 2.6 (1.2) Other Income (1.6) (3.6) (0.9) (2.8) Adoption of ASC606 (49.6) - (49.6) - Provider bonus payments - 12.1 - 12.1 Net provision of doubtful accounts (3.9) (5.3) - (1.4) Impairment of intangibles 3.8 5.8 - 2.0 Severance payments 1.4 - 1.4 - EBITDA Adjustments for recently acquired IPAs - 5.6 - 5.6 Adj. EBITDA $59.4 $60.0 $53.0 $53.6 Memo: Net Income (Loss) Attributable to Non-Controlling Interests (1) $49.4 $12.7 $48.3 $11.6

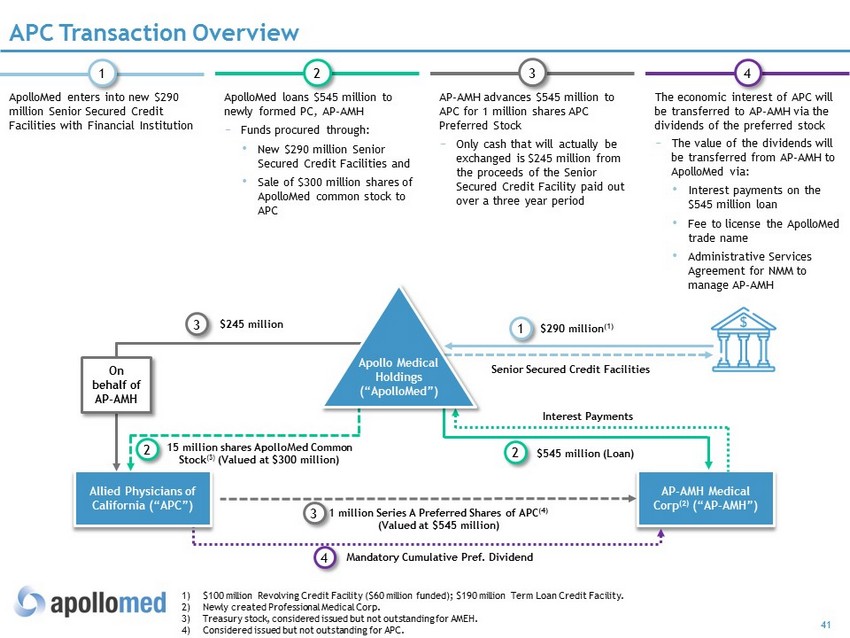

41 APC Transaction Overview 1) $ 100 million Revolving Credit Facility ($60 million funded); $190 million Term Loan Credit Facility. 2) Newly created Professional Medical Corp . 3) Treasury stock, considered issued but not outstanding for AMEH. 4) Considered issued but not outstanding for APC. ApolloMed enters into new $290 million Senior Secured Credit Facilities with Financial Institution 1 3 2 4 $545 million (Loan) Senior Secured Credit Facilities AP - AMH Medical Corp (2) (“AP - AMH”) Allied Physicians of California (“APC”) 1 million Series A Preferred Shares of APC (4) (Valued at $545 million ) $290 million (1) 15 million shares ApolloMed Common Stock (3) (Valued at $300 million) Mandatory Cumulative Pref. Dividend Interest Payments On behalf of AP - AMH $245 million Apollo Medical Holdings (“ApolloMed”) 1 2 3 3 2 4 ApolloMed loans $545 million to newly formed PC, AP - AMH − Funds procured through: • N ew $290 million Senior Secured Credit Facilities and • Sale of $300 million shares of ApolloMed common stock to APC AP - AMH advances $545 million to APC for 1 million shares APC Preferred Stock − Only cash that will actually be exchanged is $245 million from the proceeds of the Senior Secured Credit Facility paid out over a three year period The economic interest of APC will be transferred to AP - AMH via the dividends of the preferred stock − The value of the dividends will be transferred from AP - AMH to ApolloMed via: • Interest payments on the $545 million loan • Fee to license the ApolloMed trade name • Administrative Services Agreement for NMM to manage AP - AMH

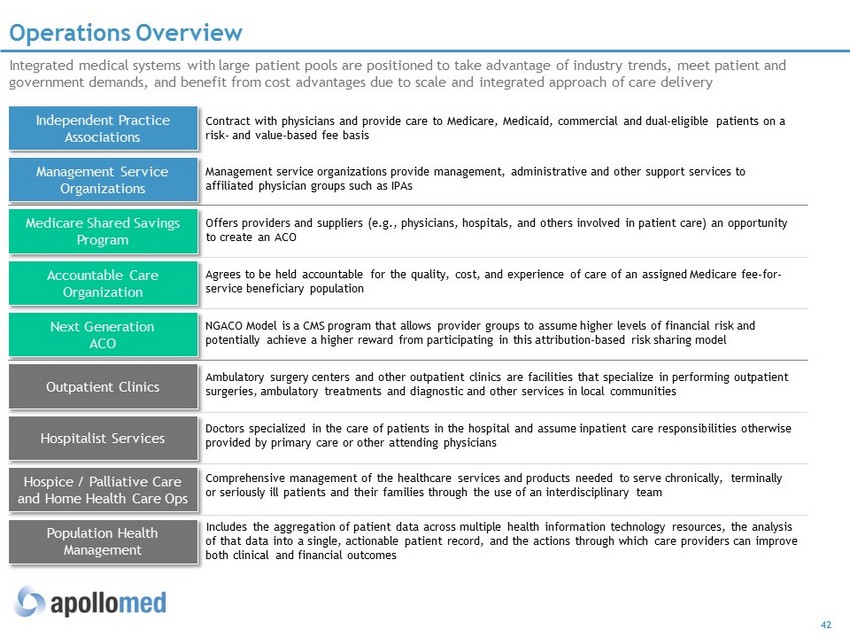

42 Operations Overview Integrated medical systems with large patient pools are positioned to take advantage of industry trends, meet patient and government demands, and benefit from cost advantages due to scale and integrated approach of care delivery Independent Practice Associations Contract with physicians and provide care to Medicare, Medicaid, commercial and dual - eligible patients on a risk - and value - based fee basis Management Service Organizations Management service organizations provide management , administrative and other support services to affiliated physician groups such as IPAs Medicare Shared Savings Program Offers providers and suppliers ( e.g ., physicians, hospitals, and others involved in patient care) an opportunity to create an ACO Accountable Care Organization Agrees to be held accountable for the quality, cost, and experience of care of an assigned Medicare fee - for - service beneficiary population Next Generation ACO NGACO Model is a CMS program that allows provider groups to assume higher levels of financial risk and potentially achieve a higher reward from participating in this attribution - based risk sharing model Outpatient Clinics Ambulatory surgery centers and other outpatient clinics are facilities that specialize in performing outpatient surgeries, ambulatory treatments and diagnostic and other services in local communities Hospitalist Services Doctors specialized in the care of patients in the hospital and assume inpatient care responsibilities otherwise provided by primary care or other attending physicians Hospice / Palliative Care and Home Health Care Ops Comprehensive management of the healthcare services and products needed to serve chronically, terminally or seriously ill patients and their families through the use of an interdisciplinary team Population Health Management Includes the aggregation of patient data across multiple health information technology resources , the analysis of that data into a single, actionable patient record, and the actions through which care providers can improve both clinical and financial outcomes

43 Key Acronyms ▪ ACO: Accountable Care Organization ▪ AIPBP: All - Inclusive Population - Based Payments ▪ APC: Allied Physicians of California IPA ▪ CMMI: Center for Medicare and Medicaid Innovation ▪ CMS : Centers for Medicare & Medicaid Services ▪ DME: Durable Medical Equipment ▪ Health Plan / Payors: Health Insurance Companies ▪ HMO: Health Maintenance Organization ▪ IPA: Independent Practice Association ▪ NCI: Non - Controlling Interest ▪ NMM: Network Medical Management ▪ MSA : Master Service Agreement ▪ MSO: Management Services Organization ▪ NGACO: Next Generation Accountable Care Organization ▪ PCP: Primary Care Physician ▪ PMPM : Per - M ember - P er - M onth ▪ SNF: Skilled Nursing Facility ▪ VIE: Variable Interest Entity