EXHIBIT 99.1

Published on March 14, 2022

Exhibit 99.1

Apollo Medical Holdings March 2022 Powered by Technology. Built by Doctors. For Patients.

This presentation contains forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 , Section 27A of the Securities Act and Section 21E of the Exchange Act. Forward - looking statements include any statements about the Compa ny's business, financial condition, operating results, plans, objectives, expectations and intentions, expansion plans, integratio n o f acquired companies and any projections of earnings, revenue, EBITDA, Adjusted EBITDA or other financial items, such as the Company's p roj ected capitation and future liquidity, and may be identified by the use of forward - looking terms such as “anticipate,” “could,” “can,” “may,” “might,” “potential,” “predict,” “should,” “estimate,” “expect,” “project,” “believe,” “plan,” “envision,” “intend,” “continu e,” “target,” “seek,” “will,” “would,” and the negative of such terms, other variations on such terms or other similar or comparable words, phrases or terminology. Forward - looking statements reflect current views with respect to future events and financial performance and theref ore cannot be guaranteed. Such statements are based on the current expectations and certain assumptions of the Company's manageme nt, and some or all of such expectations and assumptions may not materialize or may vary significantly from actual results. Actua l r esults may also vary materially from forward - looking statements due to risks, uncertainties and other factors, known and unknown, including the risk factors described from time to time in the Company’s reports to the U.S. Securities and Exchange Commission (the “SEC”), incl udi ng without limitation the risk factors discussed in the Company's Annual Report on Form 10 - K for the year ended December 31, 2021, and subsequent Quarterly Reports on Form 10 - Q. Because the factors referred to above could cause actual results or outcomes to differ materially from those expressed or imp lie d in any forward - looking statements, you should not place undue reliance on any such forward - looking statements. Any forward - looking statements speak only as of the date of this presentation and, unless legally required, the Company does not undertake any ob lig ation to update any forward - looking statement, as a result of new information, future events or otherwise. Forward - looking statements 2

Key acronyms 3 ◦ ACO: Accountable Care Organization ◦ ACO REACH: Accountable Care Organization Realizing Equity, Access, and Community Health ◦ AIPBP: All - Inclusive Population - Based Payments ◦ APC: Allied Physicians of California IPA ◦ CMMI: Center s for Medicare and Medicaid Innovation Center ◦ CMS: Centers for Medicare & Medicaid Services ◦ DC: Direct Contracting ◦ DCE: Direct Contracting Entity ◦ DME: Durable Medical Equipment ◦ Health Plan / Pay e rs: Health Insurance Companies ◦ HMO: Health Maintenance Organization ◦ IPA: Independent Practice Association ◦ NCI: Non - Controlling Interest ◦ NMM: Network Medical Management , Inc. ◦ MSA: Master Service Agreement ◦ MSO: Management Services Organization ◦ NGACO: Next Generation Accountable Care Organization ◦ PCP: Primary Care Physician ◦ PMPM: Per Member Per Month ◦ SNF: Skilled Nursing Facility ◦ VIE: Variable Interest Entity

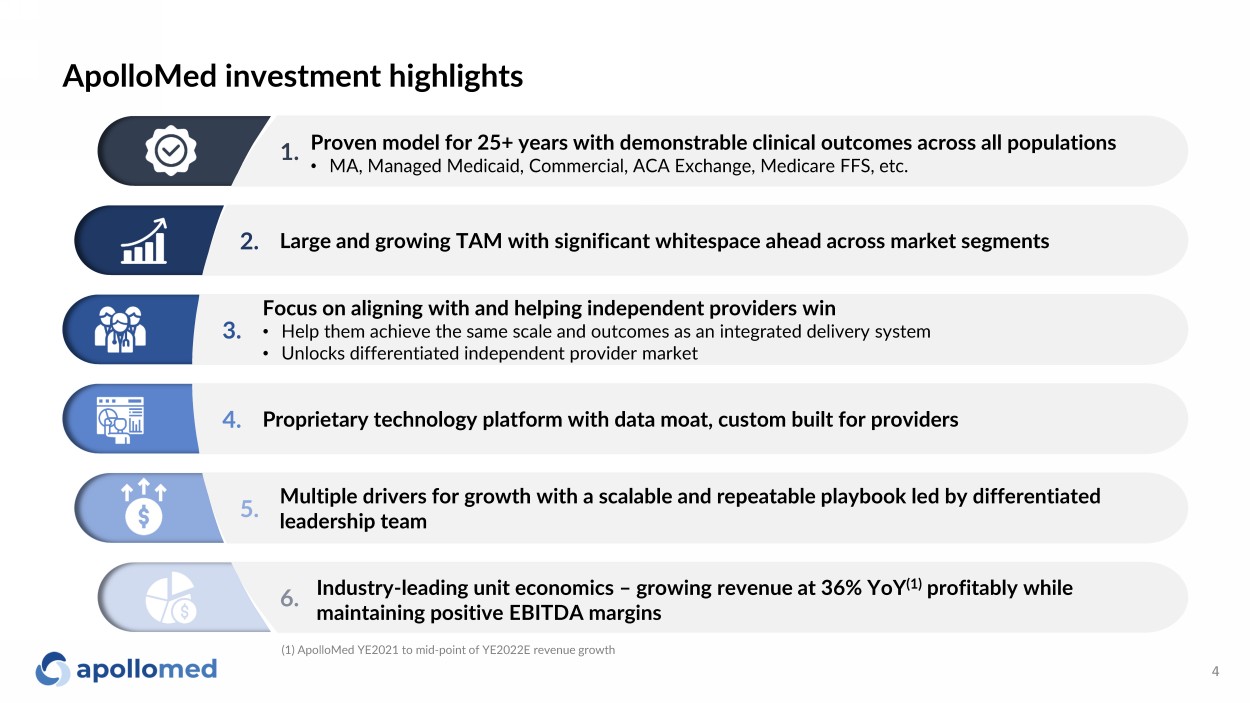

ApolloMed investment highlights 4 1. 2. 3. 5. 6. 4. Proven model for 25+ years with demonstrable clinical outcomes across all populations • MA, Managed Medicaid, Commercial, ACA Exchange, Medicare FFS, etc. Industry - leading unit economics – growing revenue at 36% YoY (1) profitably while maintaining positive EBITDA margins Focus on aligning with and helping independent providers win • Help them achieve the same scale and outcomes as an integrated delivery system • Unlocks differentiated independent provider market Proprietary technology platform with data moat, custom built for providers Multiple drivers for growth with a scalable and repeatable playbook led by differentiated leadership team Large and growing TAM with significant whitespace ahead across market segments (1) ApolloMed YE2021 to mid - point of YE2022E revenue growth

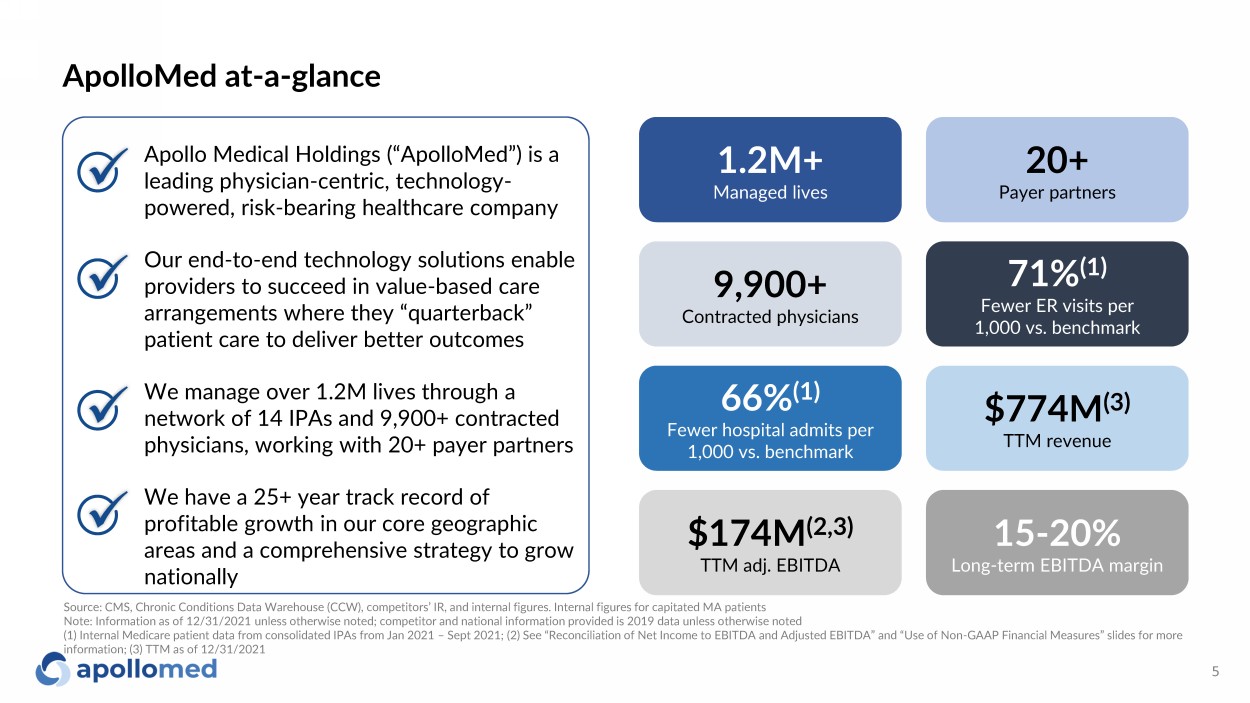

66% (1) Fewer hospital admits per 1,000 vs. benchmark $774M (3) TTM revenue $174M (2,3) TTM adj. EBITDA 15 - 20% Long - term EBITDA margin ApolloMed at - a - glance 5 71% (1) Fewer ER visits per 1,000 vs. benchmark 9,900+ Contracted physicians x x x x 1.2M+ Managed lives 20+ Payer partners Apollo Medical Holdings (“ApolloMed”) is a leading physician - centric, technology - powered, risk - bearing healthcare company Our end - to - end technology solutions enable providers to succeed in value - based care arrangements where they “quarterback” patient care to deliver better outcomes We manage over 1.2M lives through a network of 14 IPAs and 9,900+ contracted physicians, working with 20+ payer partners We have a 25+ year track record of profitable growth in our core geographic areas and a comprehensive strategy to grow nationally Source: CMS, Chronic Conditions Data Warehouse (CCW), competitors’ IR, and internal figures. Internal figures for capitated M A p atients Note: Information as of 12/31/2021 unless otherwise noted; competitor and national information provided is 2019 data unless o the rwise noted (1) Internal Medicare patient data from consolidated IPAs from Jan 2021 – Sept 2021; (2) See “Reconciliation of Net Income to EB ITDA and Adjusted EBITDA” and “Use of Non - GAAP Financial Measures” slides for more information; (3) TTM as of 12/31/2021

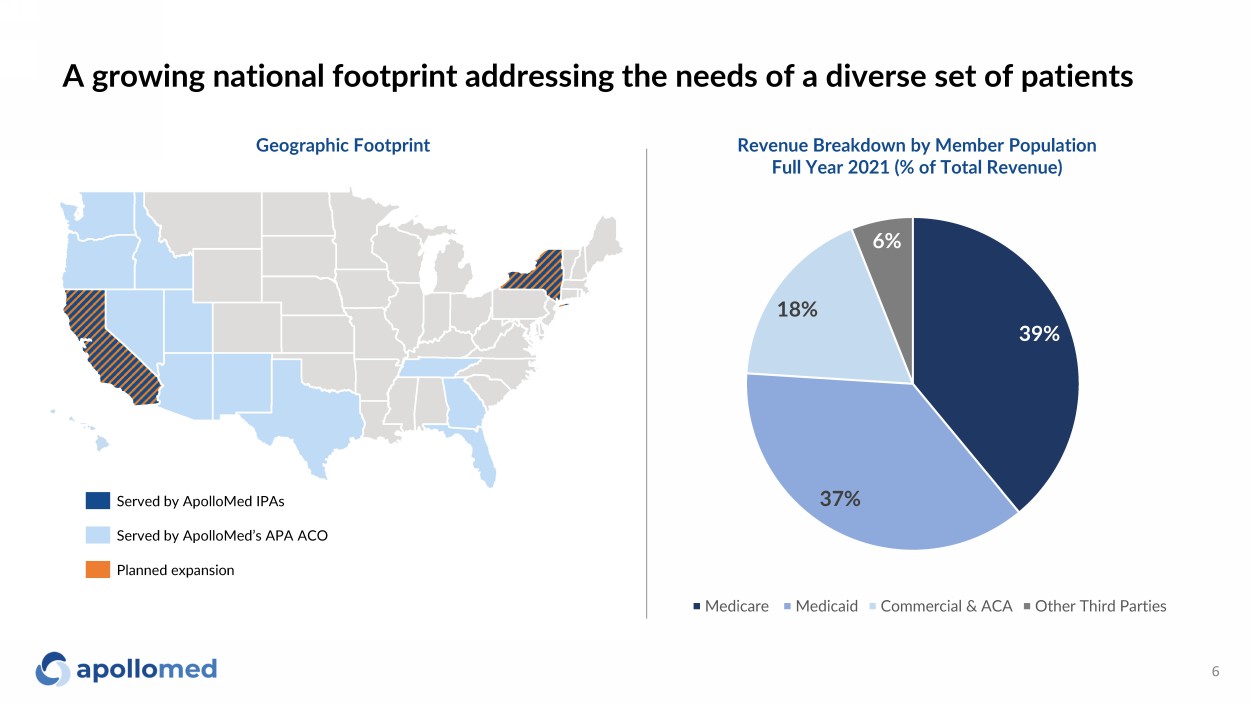

39% 37% 18% 6% Medicare Medicaid Commercial & ACA Other Third Parties A growing national footprint addressing the needs of a diverse set of patients 6 Served by ApolloMed IPAs Served by ApolloMed’s APA ACO Planned expansion Geographic Footprint Revenue Breakdown by Member Population Full Year 2021 (% of Total Revenue)

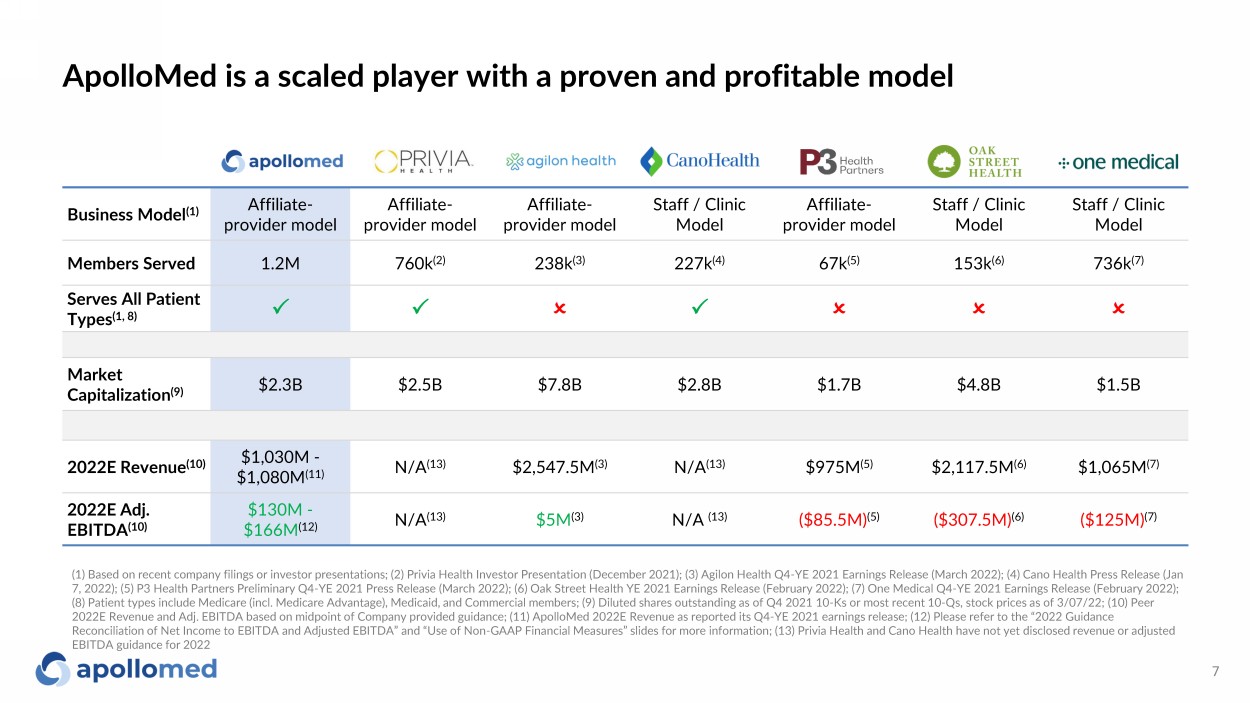

ApolloMed is a scaled player with a proven and profitable model 7 Business Model (1) Affiliate - provider model Affiliate - provider model Affiliate - provider model Staff / Clinic Model Affiliate - provider model Staff / Clinic Model Staff / Clinic Model Members Served 1.2M 760k (2) 238k (3) 227k (4) 67k (5) 153k (6) 736k (7) Serves All Patient Types (1, 8) P P O P O O O Market Capitalization (9) $2.3B $2.5B $7.8B $2.8B $1.7B $4.8B $1.5B 2022E Revenue (10) $1,030M - $1,080M (11) N /A ( 1 3 ) $2,547.5M (3) N /A ( 1 3 ) $975M (5) $2,117.5M (6) $1,065M (7) 2022E Adj. EBITDA (10) $130M - $166M (12) N/A (13) $5M (3) N/A (13) ($85.5M) (5) ($307.5M) (6) ($125M) (7) (1) Based on recent company filings or investor presentations; (2) Privia Health Investor Presentation (December 2021); (3) Agilon Health Q4 - YE 2021 Earnings Release (March 2022); (4) Cano Health Press Release (Jan 7, 2022); (5) P3 Health Partners Preliminary Q4 - YE 2021 Press Release (March 2022); (6) Oak Street Health YE 2021 Earnings Relea se (February 2022); (7) One Medical Q4 - YE 2021 Earnings Release (February 2022); (8) Patient types include Medicare (incl. Medicare Advantage), Medicaid, and Commercial members; (9) Diluted shares outstandi ng as of Q4 2021 10 - Ks or most recent 10 - Qs, stock prices as of 3/07/22; (10) Peer 2022E Revenue and Adj. EBITDA based on midpoint of Company provided guidance; (11) ApolloMed 2022E Revenue as reported its Q4 - YE 2021 earnings release; (12) Please refer to the “2022 Guidance Reconciliation of Net Income to EBITDA and Adjusted EBITDA” and “Use of Non - GAAP Financial Measures” slides for more information ; (13) Privia Health and Cano Health have not yet disclosed revenue or adjusted EBITDA guidance for 2022

Industry overview

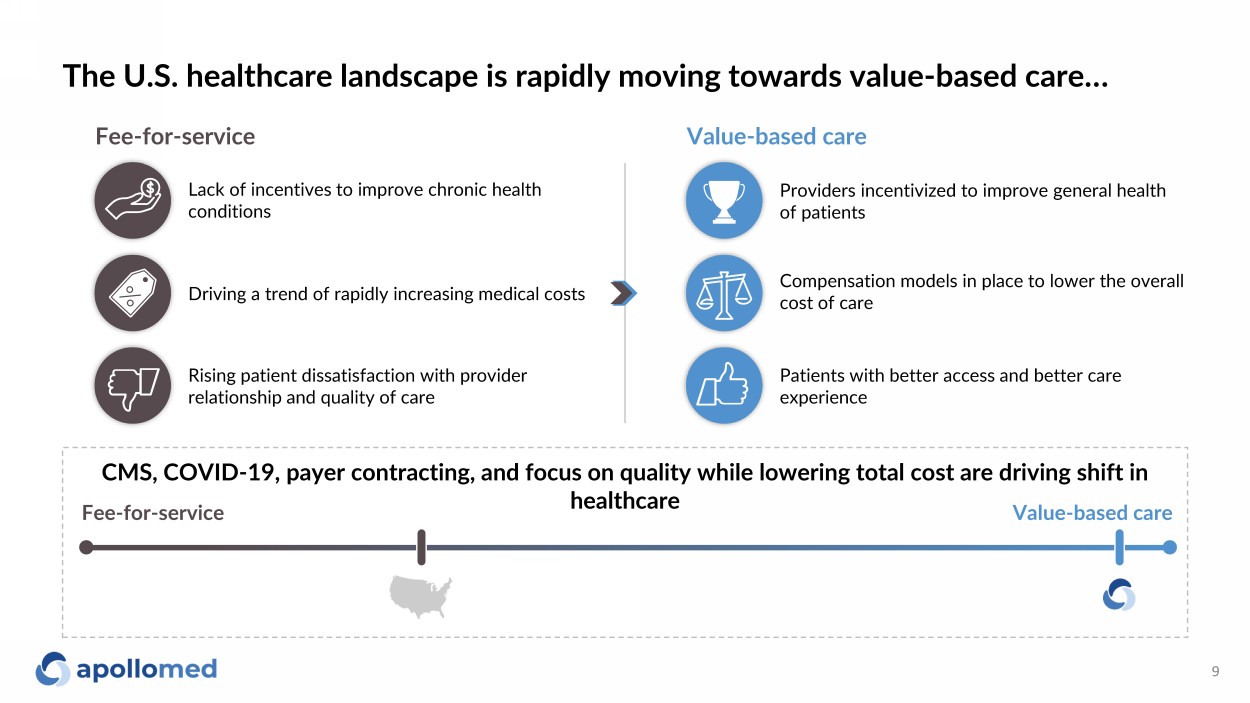

The U.S. healthcare landscape is rapidly moving towards value - based care… 9 Fee - for - service Value - based care Lack of incentives to improve chronic health conditions Driving a trend of rapidly increasing medical costs Rising patient dissatisfaction with provider relationship and quality of care Providers incentivized to improve general health of patients Compensation models in place to lower the overall cost of care Patients with better access and better care experience CMS, COVID - 19, payer contracting, and focus on quality while lowering total cost are driving shift in healthcare Value - based care Fee - for - service

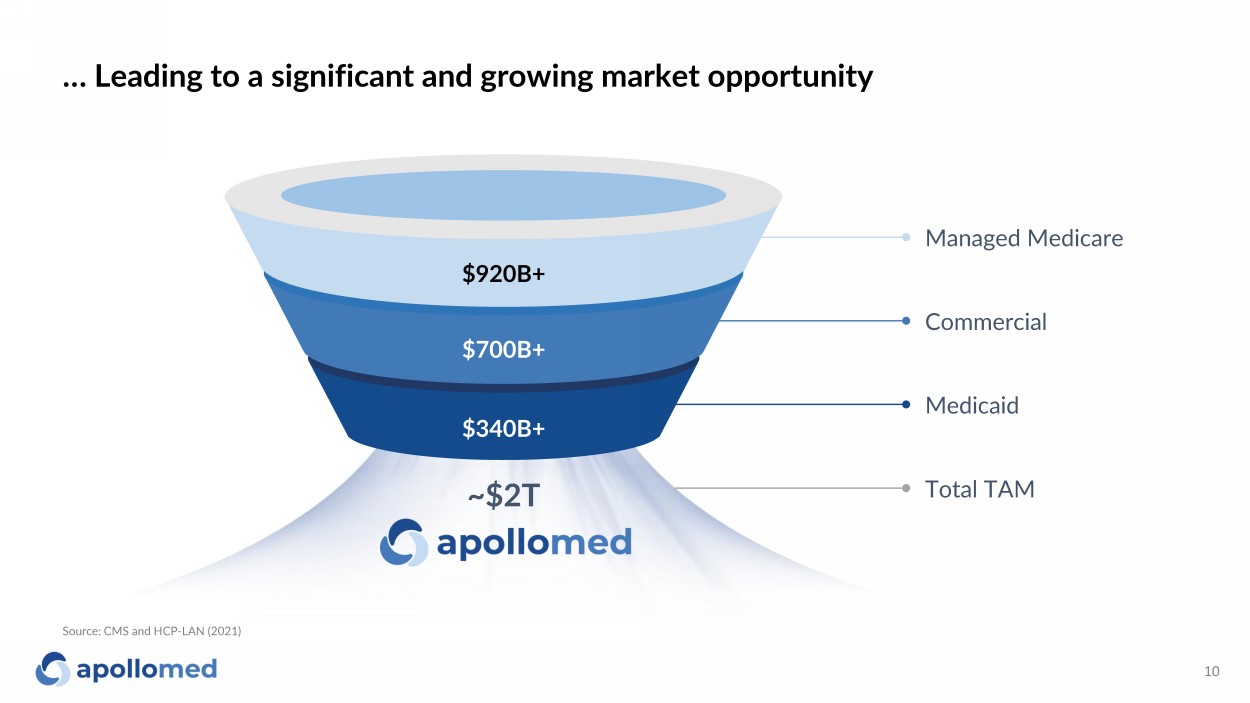

… Leading to a significant and growing market opportunity 10 Source: CMS and HCP - LAN (2021) $920B+ $700B+ $340B+ Managed Medicare Commercial Medicaid Total TAM ~$2T

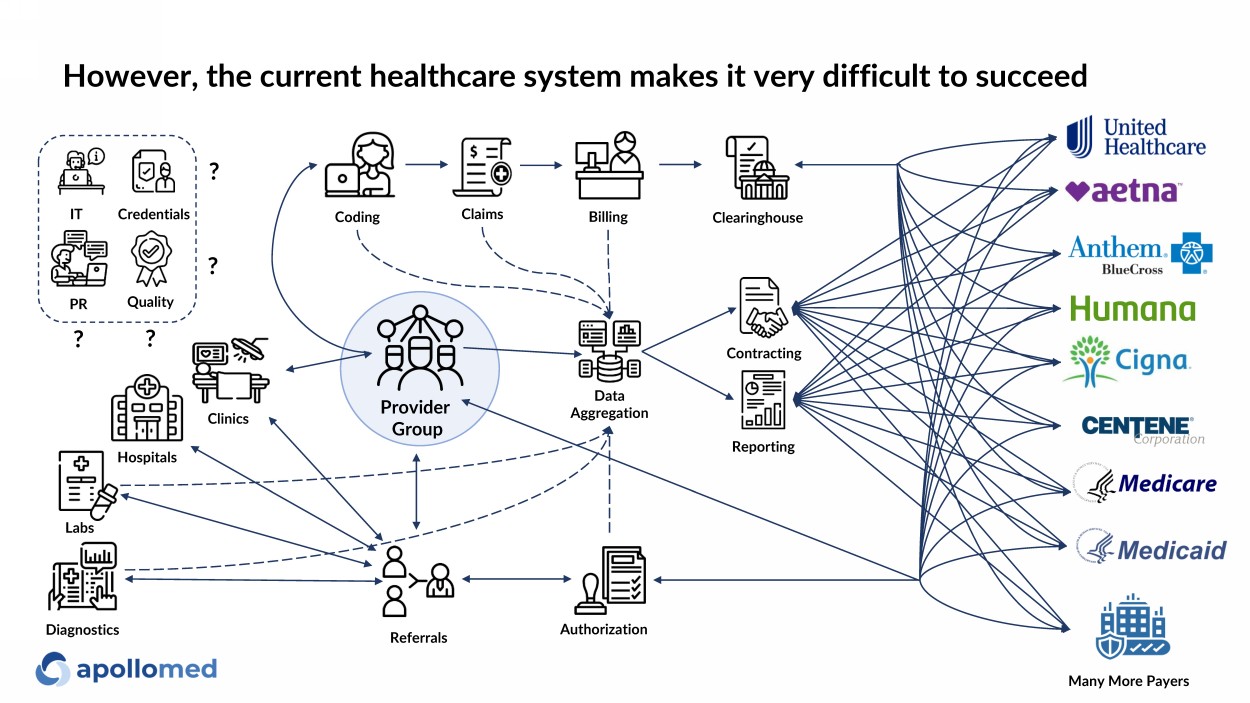

Reporting Contracting Claims Data Aggre gation Billing Coding Hospitals Clinics Referrals Provider Group Authorization Clearinghouse IT Credentials PR Quality ? ? ? ? Labs Many More Payers Diagnostics However, the current healthcare system makes it very difficult to succeed

Platform overview

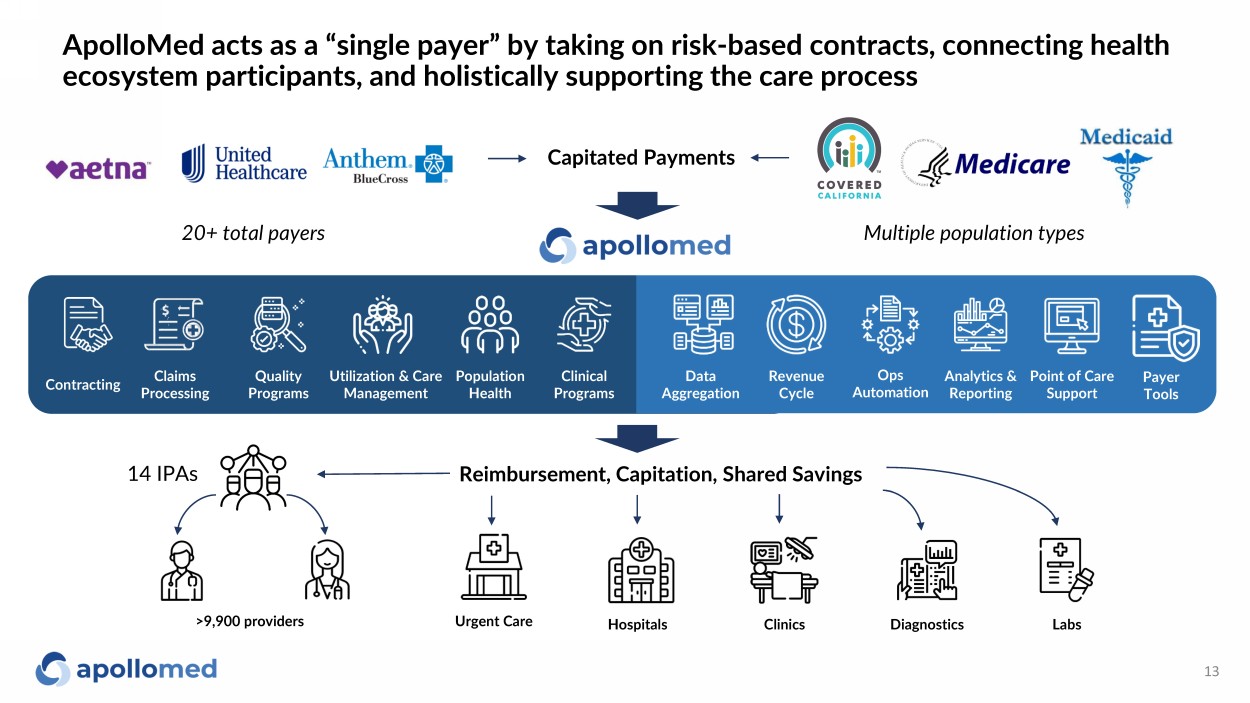

ApolloMed acts as a “single payer” by taking on risk - based contracts, connecting health ecosystem participants, and holistically supporting the care process 13 Capitated Payments Utilization & Care Management Claims Processing Ops Automation Point of Care Support Analytics & Reporting Contracting Clinical Programs Quality Programs Population Health Data Aggregation Revenue Cycle P ayer Tools Reimbursement, Capitation, Shared Savings >9,900 providers Hospitals Labs Urgent Care Clinics Diagnostics 20+ total payers 14 IPAs Multiple population types

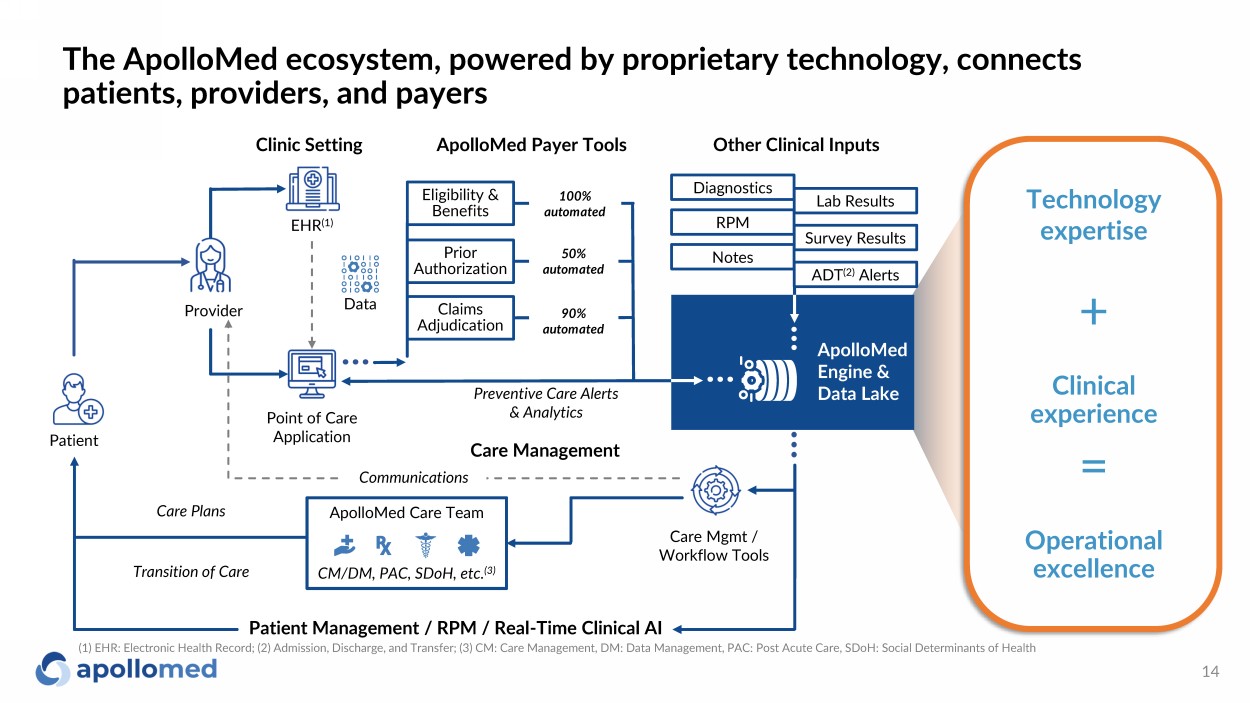

The ApolloMed ecosystem, powered by proprietary technology, connects patients, providers, and payers 14 Provider Point of Care Application EHR (1) Data Patient Care Management ApolloMed Care Team CM/DM, PAC, SDoH , etc. (3) Communications Patient Management / RPM / Real - Time Clinical AI Care Mgmt / Workflow Tools Eligibility & Benefits Claims Adjudication Prior Authorization ApolloMed Payer Tools Other Clinical Inputs Clinic Setting 100% automated 50% automated 90% automated Technology expertise Operational excellence Clinical experience + = ApolloMed Engine & Data Lake (1) EHR: Electronic Health Record; (2) Admission, Discharge, and Transfer; (3) CM: Care Management, DM: Data Management, PAC: Po st Acute Care, SDoH : Social Determinants of Health Care Plans Transition of Care Preventive Care Alerts & Analytics RPM Notes ADT (2) Alerts Diagnostics Lab Results Survey Results

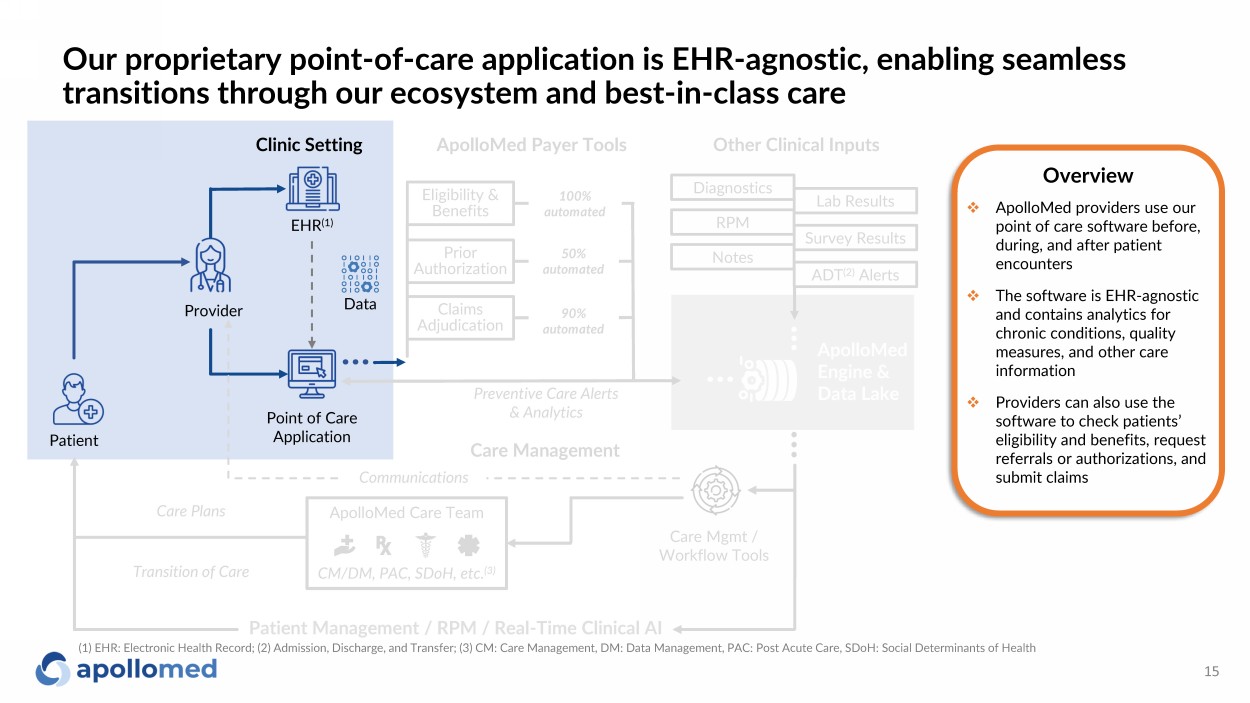

ApolloMed Care Team Our proprietary point - of - care application is EHR - agnostic, enabling seamless transitions through our ecosystem and best - in - class care 15 Provider Point of Care Application Data Patient Care Management Clinic Setting CM/DM, PAC, SDoH , etc. (3) Communications Care Mgmt / Workflow Tools Other Clinical Inputs Overview □ ApolloMed providers use our point of care software before, during, and after patient encounters □ The software is EHR - agnostic and contains analytics for chronic conditions, quality measures, and other care information □ Providers can also use the software to check patients’ eligibility and benefits, request referrals or authorizations, and submit claims Eligibility & Benefits Claims Adjudication Prior Authorization 100% automated 50% automated 90% automated ApolloMed Payer Tools ApolloMed Engine & Data Lake EHR (1) Care Plans Transition of Care Preventive Care Alerts & Analytics RPM Notes ADT (2) Alerts Diagnostics Lab Results Survey Results Patient Management / RPM / Real - Time Clinical AI (1) EHR: Electronic Health Record; (2) Admission, Discharge, and Transfer; (3) CM: Care Management, DM: Data Management, PAC: Po st Acute Care, SDoH : Social Determinants of Health

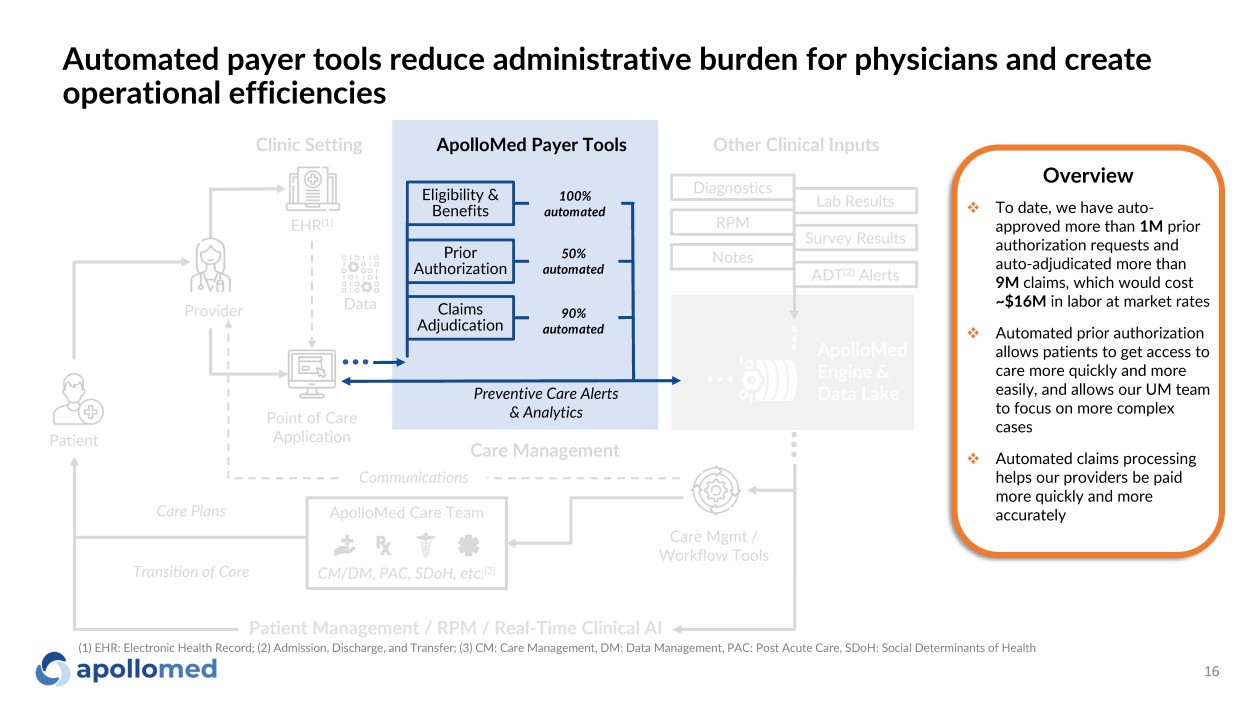

ApolloMed Care Team Automated payer tools reduce administrative burden for physicians and create operational efficiencies 16 Provider Point of Care Application EHR (1) Data Patient Care Management CM/DM, PAC, SDoH , etc. (3) Communications Care Mgmt / Workflow Tools Preventive Care Alerts & Analytics Other Clinical Inputs Clinic Setting Overview □ To date, we have auto - approved more than 1M prior authorization requests and auto - adjudicated more than 9M claims, which would cost ~$16M in labor at market rates □ Automated prior authorization allows patients to get access to care more quickly and more easily, and allows our UM team to focus on more complex cases □ Automated claims processing helps our providers be paid more quickly and more accurately Eligibility & Benefits Claims Adjudication Prior Authorization ApolloMed Payer Tools 100% automated 50% automated 90% automated ApolloMed Engine & Data Lake Care Plans Transition of Care RPM Notes ADT (2) Alerts Diagnostics Lab Results Survey Results Patient Management / RPM / Real - Time Clinical AI (1) EHR: Electronic Health Record; (2) Admission, Discharge, and Transfer; (3) CM: Care Management, DM: Data Management, PAC: Po st Acute Care, SDoH : Social Determinants of Health

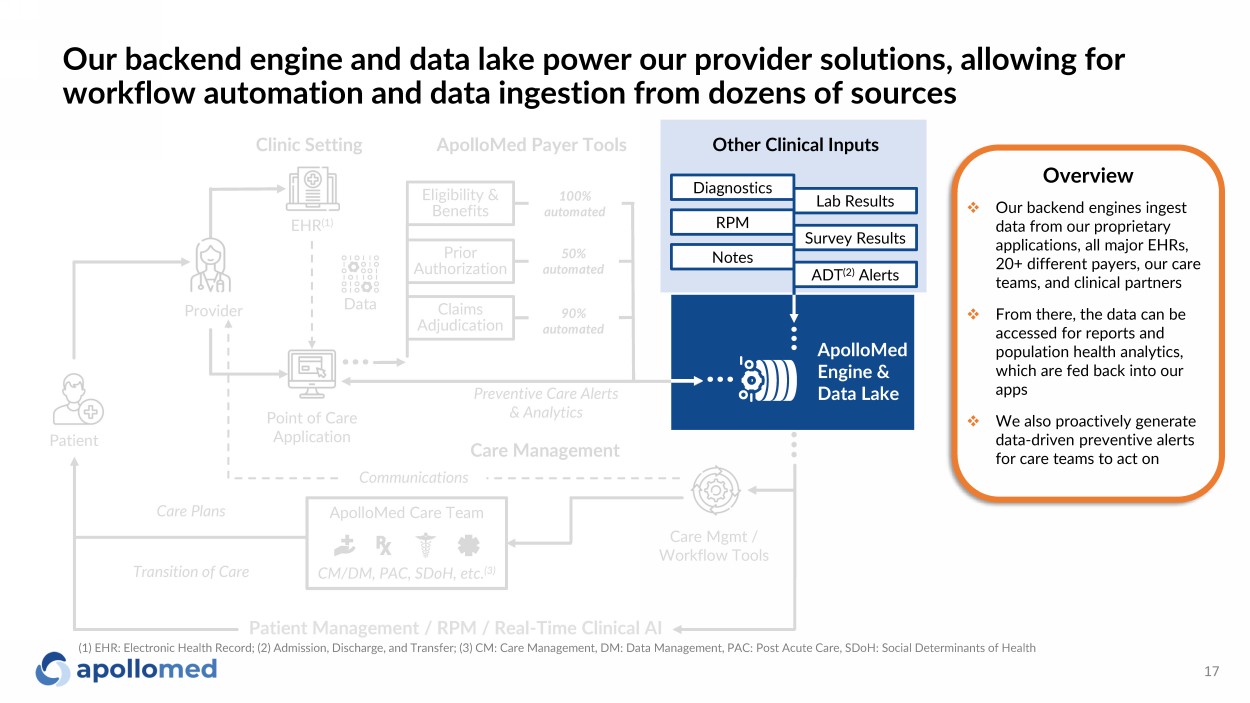

ApolloMed Care Team Our backend engine and data lake power our provider solutions, allowing for workflow automation and data ingestion from dozens of sources 17 Provider Point of Care Application Data Patient Care Management Communications Care Mgmt / Workflow Tools ApolloMed Engine & Data Lake Preventive Care Alerts & Analytics Other Clinical Inputs Clinic Setting CM/DM, PAC, SDoH , etc. (3) Overview □ Our backend engines ingest data from our proprietary applications, all major EHRs, 20+ different payers, our care teams, and clinical partners □ From there, the data can be accessed for reports and population health analytics, which are fed back into our apps □ We also proactively generate data - driven preventive alerts for care teams to act on Eligibility & Benefits Claims Adjudication Prior Authorization 100% automated 50% automated 90% automated ApolloMed Payer Tools EHR (1) Care Plans Transition of Care RPM Notes ADT (2) Alerts Diagnostics Lab Results Survey Results Patient Management / RPM / Real - Time Clinical AI (1) EHR: Electronic Health Record; (2) Admission, Discharge, and Transfer; (3) CM: Care Management, DM: Data Management, PAC: Po st Acute Care, SDoH : Social Determinants of Health

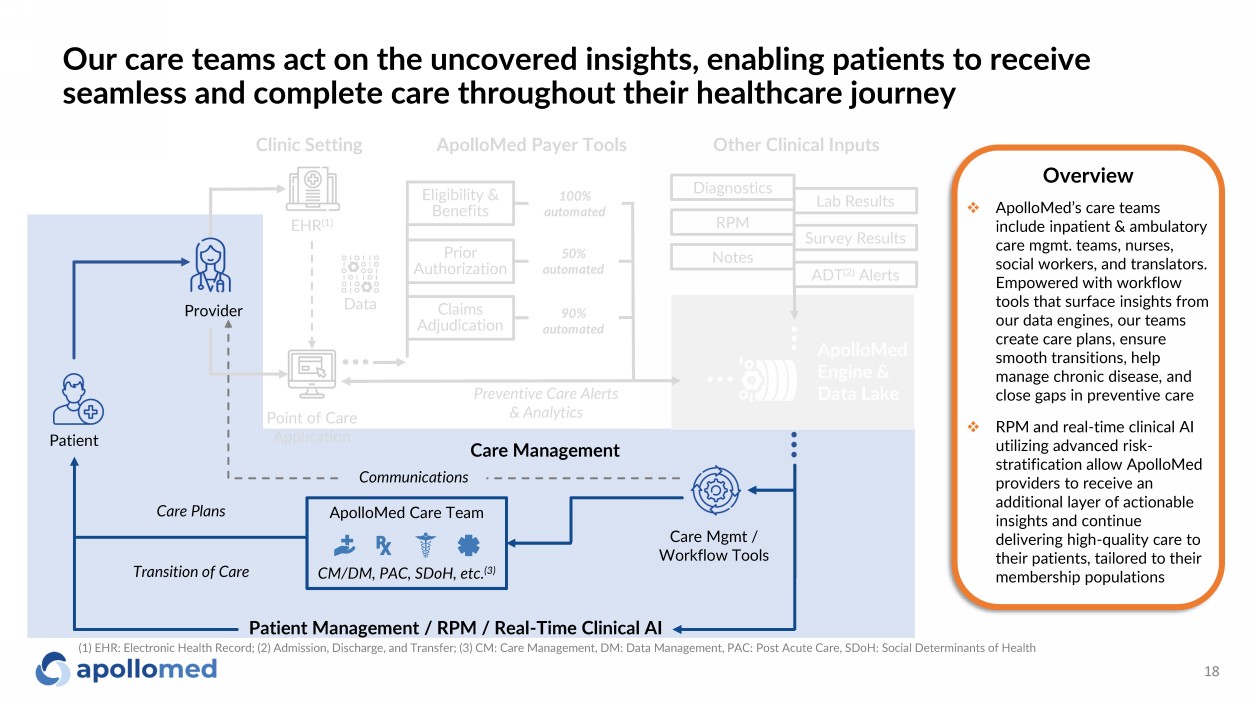

Our care teams act on the uncovered insights, enabling patients to receive seamless and complete care throughout their healthcare journey 18 Provider Point of Care Application Data Patient Care Management ApolloMed Care Team CM/DM, PAC, SDoH , etc. (3) Communications Care Mgmt / Workflow Tools ApolloMed Engine & Data Lake Preventive Care Alerts & Analytics Other Clinical Inputs Clinic Setting Overview □ ApolloMed’s care teams include inpatient & ambulatory care mgmt. teams, nurses, social workers, and translators. Empowered with workflow tools that surface insights from our data engines, our teams create care plans, ensure smooth transitions, help manage chronic disease, and close gaps in preventive care □ RPM and real - time clinical AI utilizing advanced risk - stratification allow ApolloMed providers to receive an additional layer of actionable insights and continue delivering high - quality care to their patients, tailored to their membership populations Eligibility & Benefits Claims Adjudication Prior Authorization 100% automated 50% automated 90% automated ApolloMed Payer Tools EHR (1) Care Plans Transition of Care RPM Notes ADT (2) Alerts Diagnostics Lab Results Survey Results Patient Management / RPM / Real - Time Clinical AI (1) EHR: Electronic Health Record; (2) Admission, Discharge, and Transfer; (3) CM: Care Management, DM: Data Management, PAC: Po st Acute Care, SDoH : Social Determinants of Health

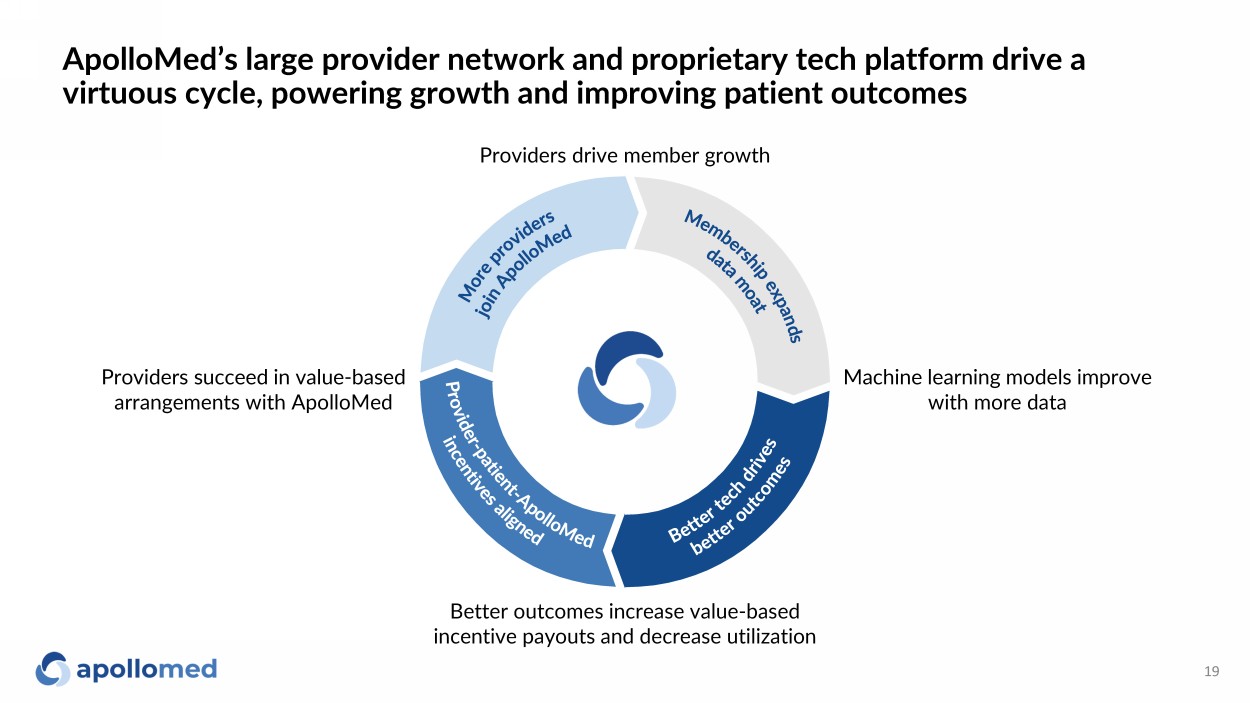

ApolloMed’s large provider network and proprietary tech platform drive a virtuous cycle, powering growth and improving patient outcomes 19 Better outcomes increase value - based incentive payouts and decrease utilization Machine learning models improve with more data Providers succeed in value - based arrangements with ApolloMed Providers drive member growth

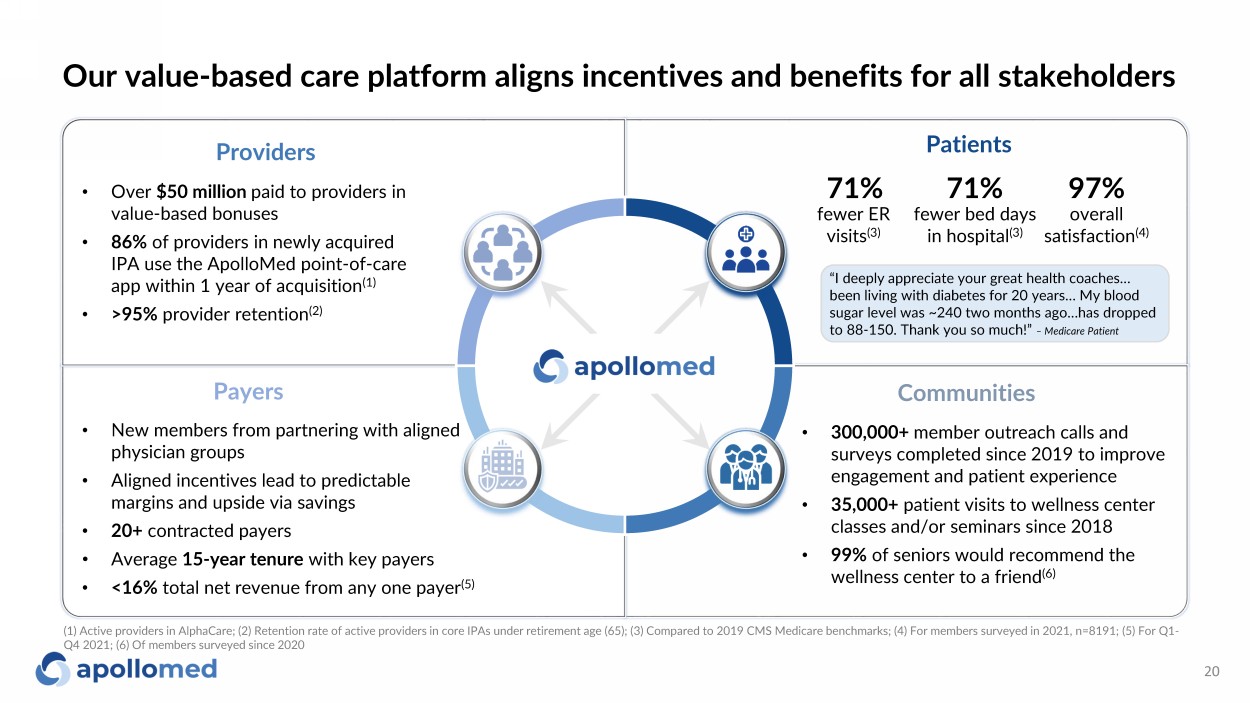

Our value - based care platform aligns incentives and benefits for all stakeholders 20 • 300,000+ member outreach calls and surveys completed since 2019 to improve engagement and patient experience • 35,000+ patient visits to wellness center classes and/or seminars since 2018 • 99% of seniors would recommend the wellness center to a friend (6) Communities Patients • New members from partnering with aligned physician groups • Aligned incentives lead to predictable margins and upside via savings • 20+ contracted payers • Average 15 - year tenure with key payers • <16% total net revenue from any one payer (5) Payers • Over $50 million paid to providers in value - based bonuses • 86% of providers in newly acquired IPA use the ApolloMed point - of - care app within 1 year of acquisition (1) • >95% provider retention (2) Providers “I deeply appreciate your great health coaches… been living with diabetes for 20 years… My blood sugar level was ~240 two months ago…has dropped to 88 - 150. Thank you so much!” – Medicare Patient 71% fewer ER visits (3) 71% fewer bed days in hospital (3) 97% overall satisfaction (4) (1) Active providers in AlphaCare ; (2) Retention rate of active providers in core IPAs under retirement age (65); (3) Compared to 2019 CMS Medicare benchmarks ; ( 4) For members surveyed in 2021, n=8191; (5) For Q1 - Q4 2021; (6) Of members surveyed since 2020

Clinical and financial outcomes

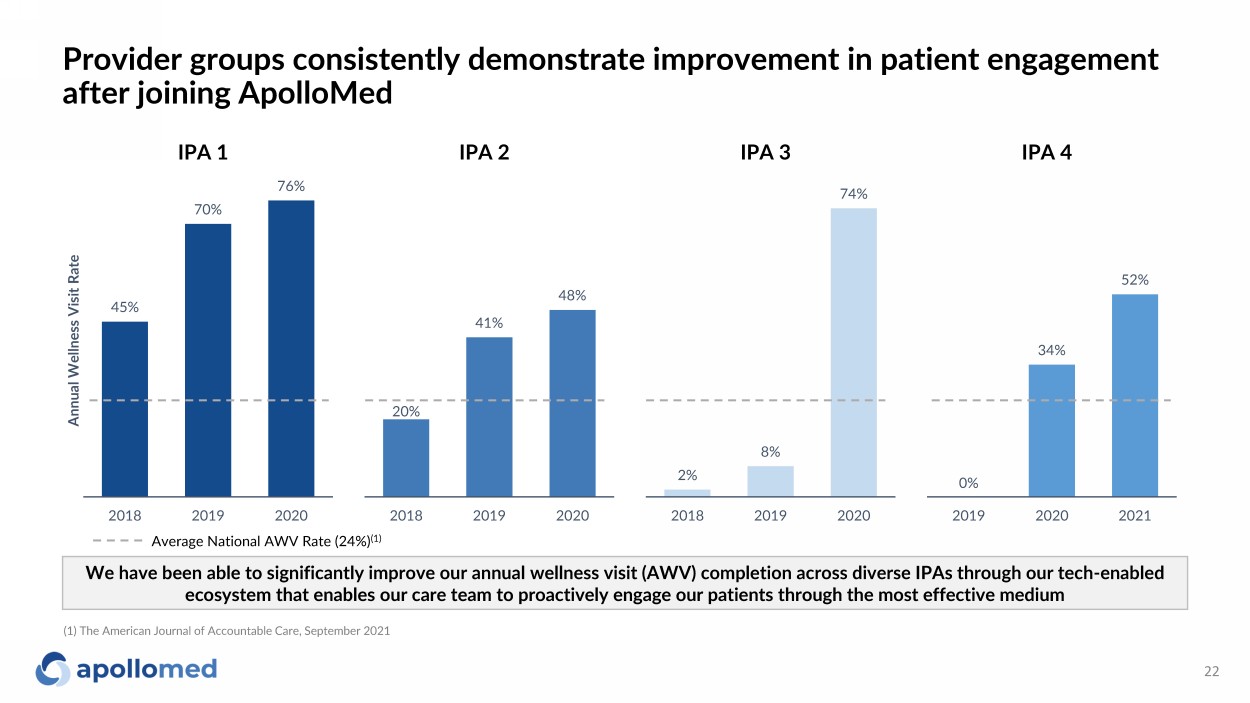

Provider groups consistently demonstrate improvement in patient engagement after joining ApolloMed 22 45% 70% 76% 2018 2019 2020 Annual Wellness Visit Rate IPA 1 IPA 2 IPA 3 IPA 4 20% 41% 48% 2018 2019 2020 2% 8% 74% 2018 2019 2020 0% 34% 52% 2019 2020 2021 We have been able to significantly improve our annual wellness visit (AWV) completion across diverse IPAs through our tech - enabl ed ecosystem that enables our care team to proactively engage our patients through the most effective medium Average National AWV Rate (24%) (1) (1) The American Journal of Accountable Care, September 2021

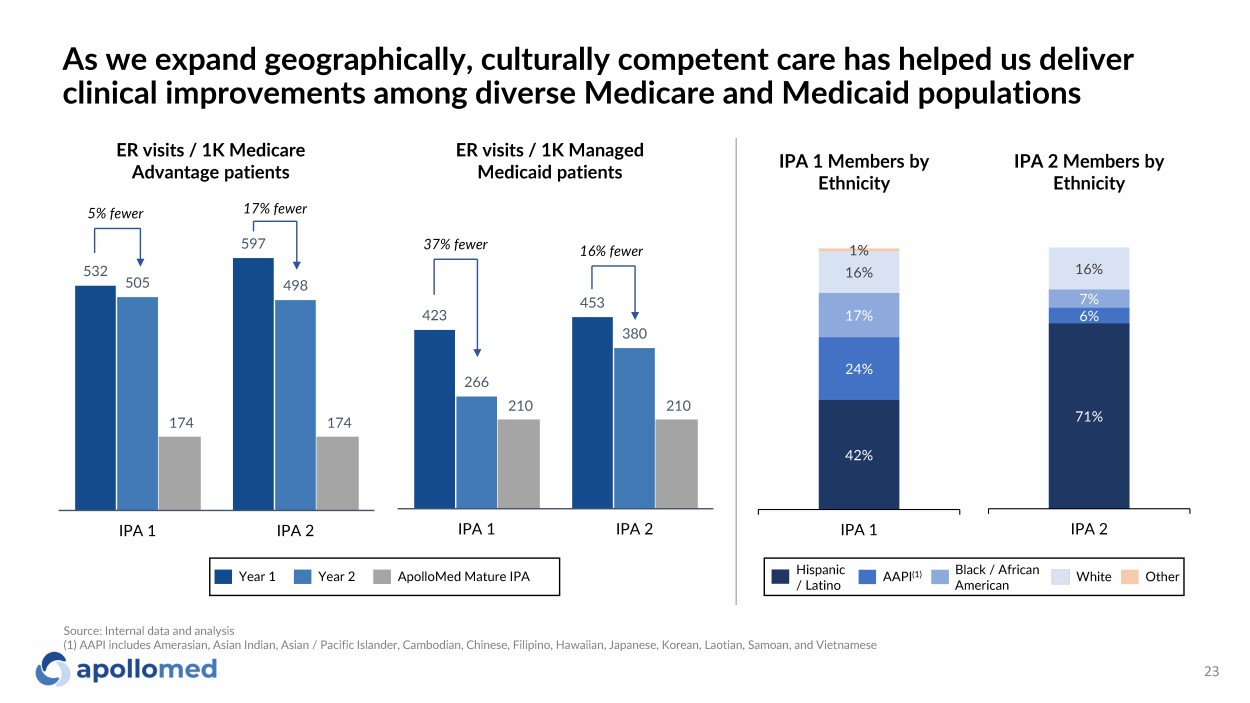

532 597 505 498 174 174 IPA 1 IPA 2 As we expand geographically, culturally competent care has helped us deliver clinical improvements among diverse Medicare and Medicaid populations 23 ER visits / 1K Medicare Advantage patients ER visits / 1K Managed Medicaid patients 423 453 266 380 210 210 IPA 1 IPA 2 42% 24% 17% 16% 1% IPA 1 71% 6% 7% 16% IPA 2 IPA 1 Members by Ethnicity IPA 2 Members by Ethnicity Year 1 Year 2 ApolloMed Mature IPA Hispanic / Latino AAPI (1) Black / African American White Other 5% fewer 17% fewer 37% fewer 16% fewer Source: Internal data and analysis (1) AAPI includes Amerasian , Asian Indian, Asian / Pacific Islander, Cambodian, Chinese, Filipino, Hawaiian, Japanese, Korean, Laotian, Samoan, and Viet nam ese

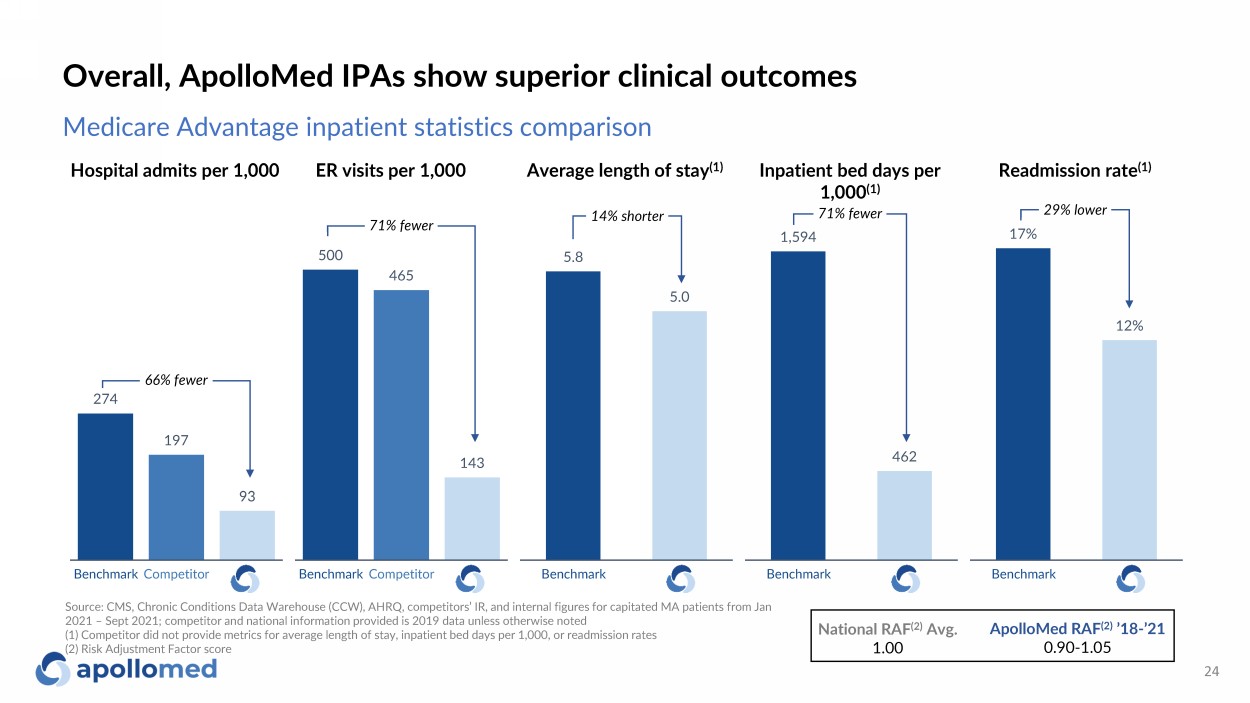

Overall, ApolloMed IPAs show superior clinical outcomes 24 National RAF (2) Avg. 1.00 ApolloMed RAF (2) ’18 - ’21 0.90 - 1.05 Medicare Advantage inpatient statistics comparison Hospital admits per 1,000 ER visits per 1,000 Average length of stay (1) Inpatient bed days per 1,000 (1) Readmission rate (1) 274 197 93 Benchmark Competitor 66 % fewer 500 465 143 Benchmark Competitor 71 % fewer 5.8 5.0 Benchmark 14 % shorter 1,594 462 Benchmark 71 % fewer 17% 12% Benchmark 29 % lower Source: CMS, Chronic Conditions Data Warehouse (CCW), AHRQ, competitors’ IR, and internal figures for capitated MA patients f rom Jan 2021 – Sept 2021; competitor and national information provided is 2019 data unless otherwise noted (1) Competitor did not provide metrics for average length of stay, inpatient bed days per 1,000, or readmission rates (2) Risk Adjustment Factor score

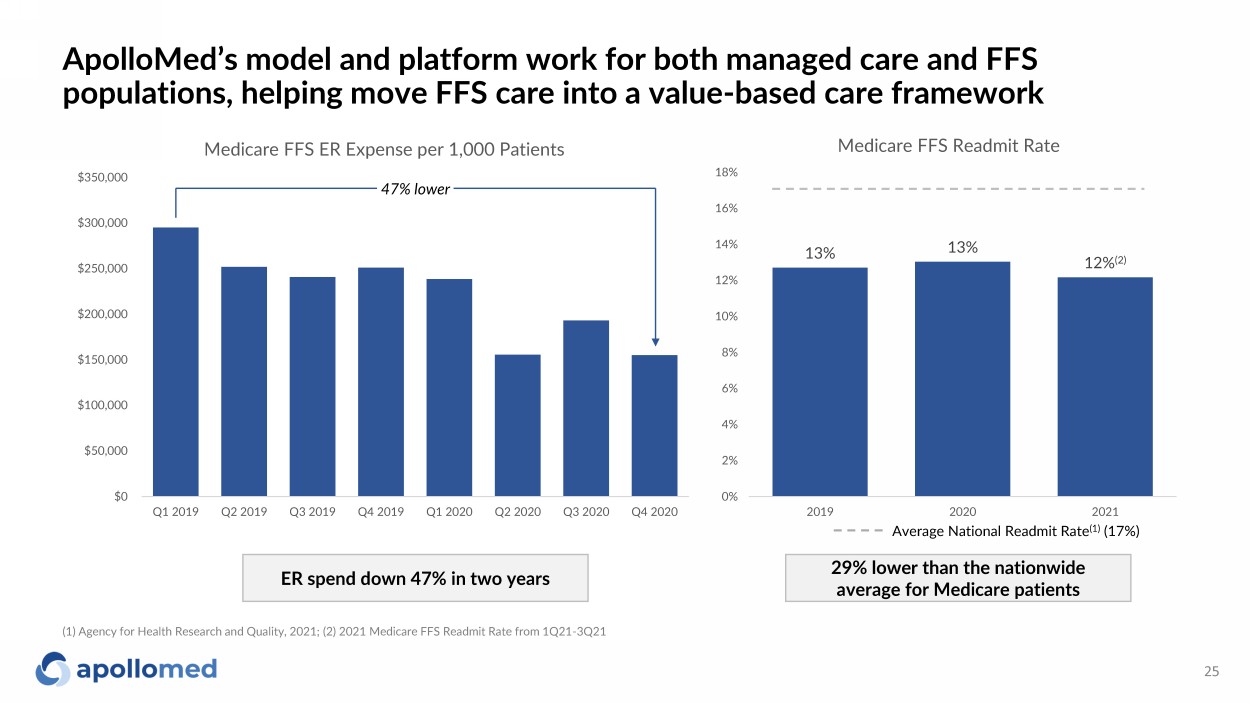

ApolloMed’s model and platform work for both managed care and FFS populations, helping move FFS care into a value - based care framework 25 $0 $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Medicare FFS ER Expense per 1,000 Patients 47% lower 13% 13% 12% (2) 0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 2019 2020 2021 Medicare FFS Readmit Rate Average National Readmit Rate (1) (17%) (1) Agency for Health Research and Quality, 2021; (2) 2021 Medicare FFS Readmit Rate from 1Q21 - 3Q21 ER spend down 47% in two years 29% lower than the nationwide average for Medicare patients

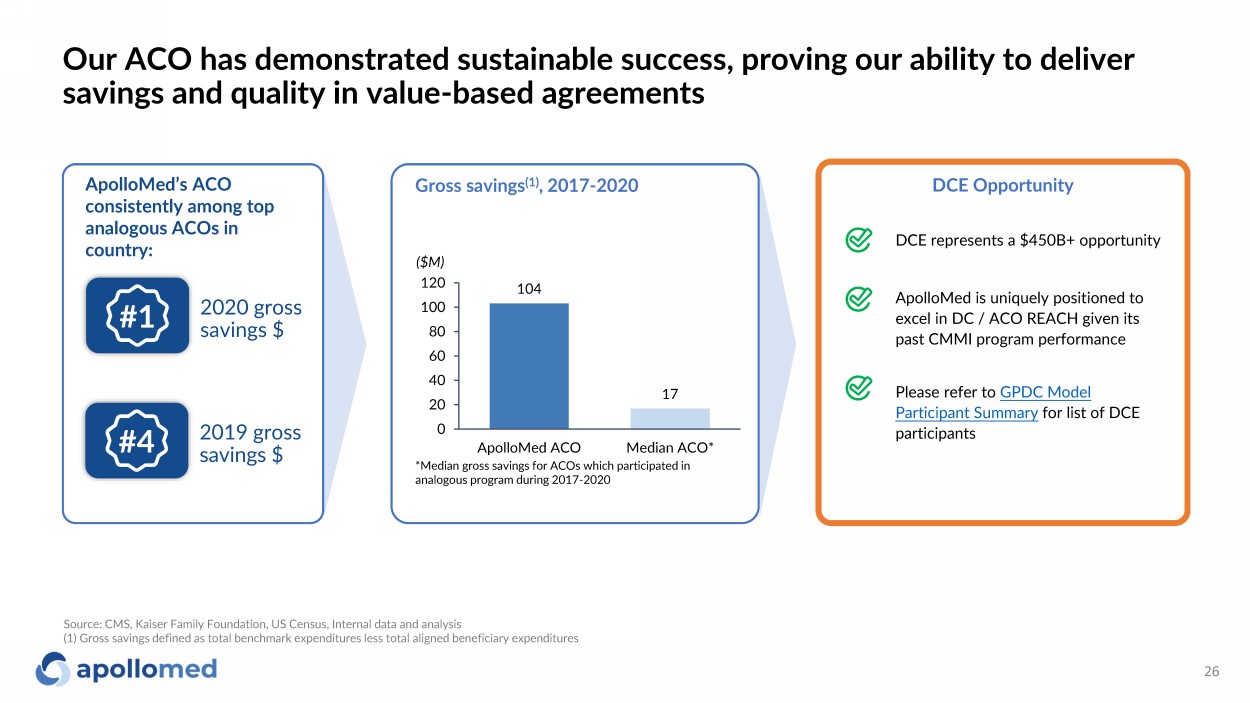

Our ACO has demonstrated sustainable success, proving our ability to deliver savings and quality in value - based agreements 26 ApolloMed’s ACO consistently among top analogous ACOs in country: 2020 gross savings $ 2019 gross savings $ Gross savings (1) , 2017 - 2020 *Median gross savings for ACOs which participated in analogous program during 2017 - 2020 104 17 0 20 40 60 80 100 120 ApolloMed ACO Median ACO* ($M) #1 #4 Source: CMS, Kaiser Family Foundation, US Census, Internal data and analysis (1) Gross savings defined as total benchmark expenditures less total aligned beneficiary expenditures DCE represents a $450B+ opportunity DCE Opportunity ApolloMed is uniquely positioned to excel in DC / ACO REACH given its past CMMI program performance Please refer to GPDC Model Participant Summary for list of DCE participants

Growth strategy

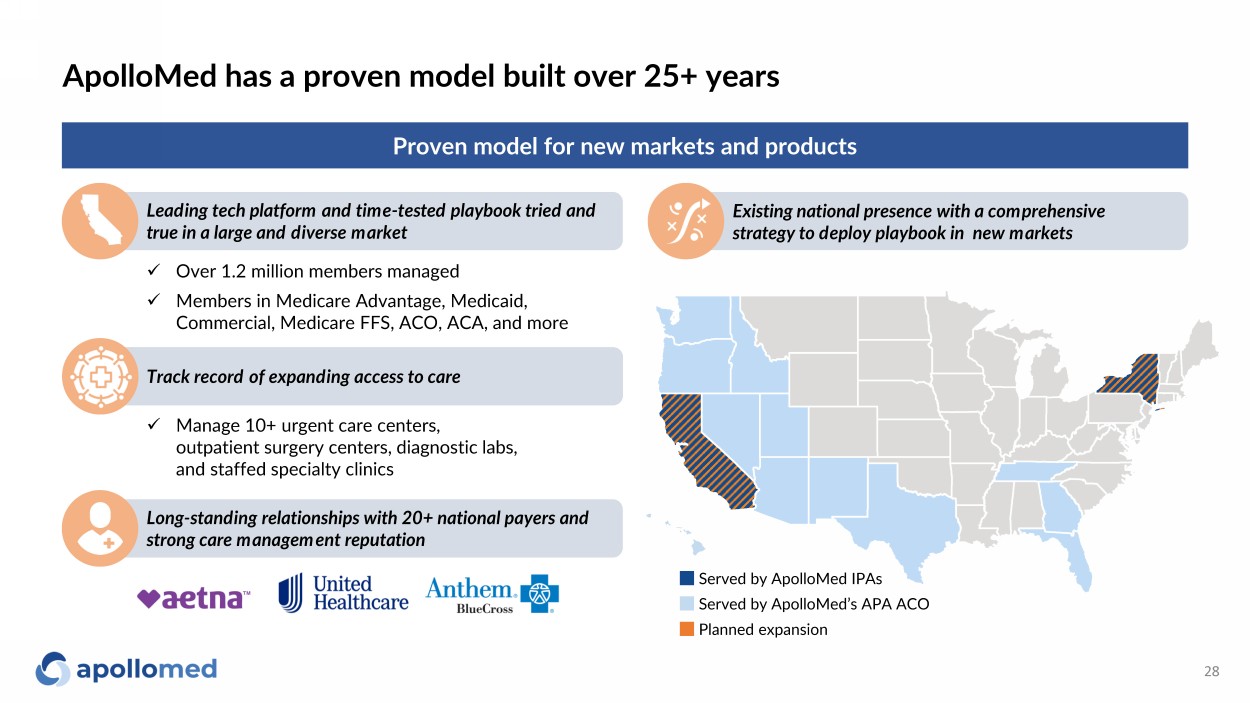

ApolloMed has a proven model built over 25+ years 28 Leading tech platform and time - tested playbook tried and true in a large and diverse market Existing national presence with a comprehensive strategy to deploy playbook in new markets x Over 1.2 million members managed x Members in Medicare Advantage, Medicaid, Commercial, Medicare FFS, ACO, ACA, and more Proven model for new markets and products Long - standing relationships with 20+ national payers and strong care management reputation Served by ApolloMed IPAs Served by ApolloMed’s APA ACO Planned expansion Track record of expanding access to care x Manage 10+ urgent care centers, outpatient surgery centers, diagnostic labs, and staffed specialty clinics

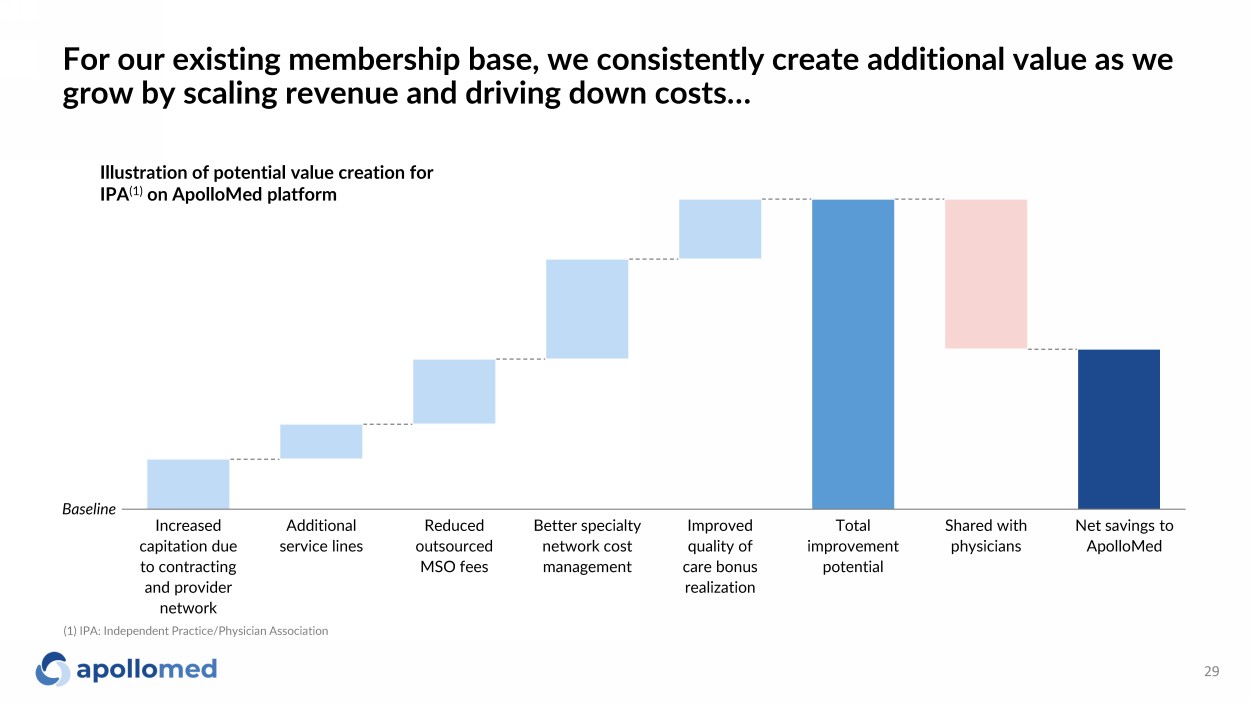

For our existing membership base, we consistently create additional value as we grow by scaling revenue and driving down costs… 29 Increased capitation due to contracting and provider network Better specialty network cost management Additional service lines Reduced outsourced MSO fees Improved quality of care bonus realization Total improvement potential Shared with physicians Net savings to ApolloMed Illustration of potential value creation for IPA (1) on ApolloMed platform Baseline (1) IPA: Independent Practice/Physician Association

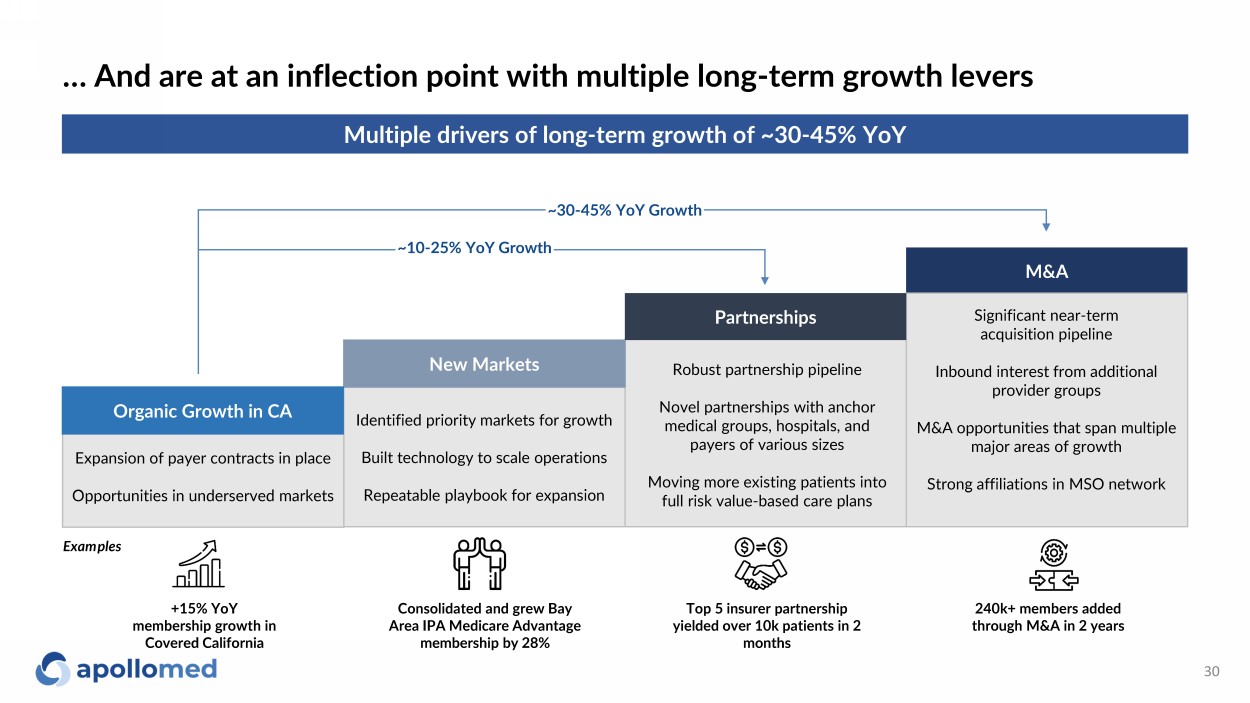

… And are at an inflection point with multiple long - term growth levers 30 Multiple drivers of long - term growth of ~30 - 45% YoY +15% YoY membership growth in Covered California Consolidated and grew Bay Area IPA Medicare Advantage membership by 28% Top 5 insurer partnership yielded over 10k patients in 2 months 240k+ members added through M&A in 2 years M&A Significant near - term acquisition pipeline Inbound interest from additional provider groups M&A opportunities that span multiple major areas of growth Strong affiliations in MSO network Identified priority markets for growth Built technology to scale operations Repeatable playbook for expansion Expansion of payer contracts in place Opportunities in underserved markets Robust partnership pipeline Novel partnerships with anchor medical groups, hospitals, and payers of various sizes Moving more existing patients into full risk value - based care plans New Markets Partnerships Examples ~10 - 25% YoY Growth ~30 - 45% YoY Growth Organic Growth in CA

Financials

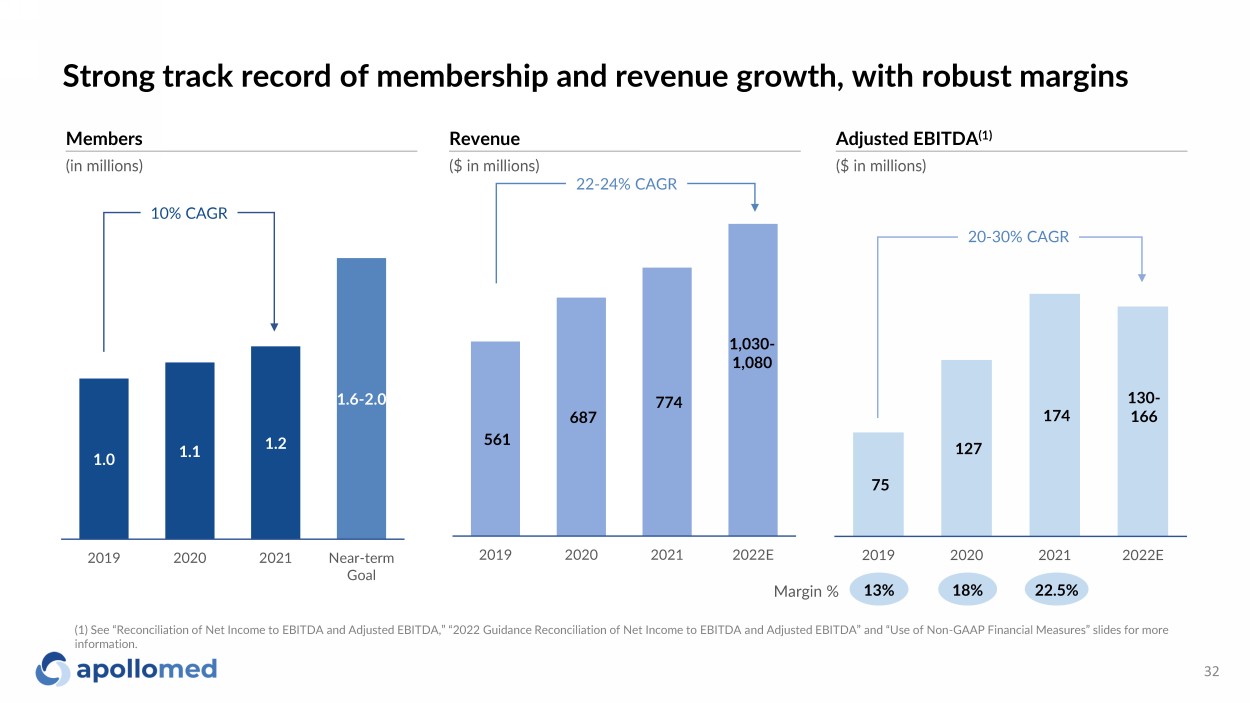

75 127 174 2019 2020 2021 2022E 1.0 1.1 1.2 1.6 - 2.0 2019 2020 2021 Near-term Goal Strong track record of membership and revenue growth, with robust margins 32 17% (in millions) ($ in millions) Members Revenue 561 687 774 2019 2020 2021 2022E 22 - 24% CAGR 10% CAGR ($ in millions) Adjusted EBITDA (1) 20 - 30% CAGR Margin % 18% 22.5% 13% (1) See “Reconciliation of Net Income to EBITDA and Adjusted EBITDA,” “2022 Guidance Reconciliation of Net Income to EBITDA a nd Adjusted EBITDA” and “Use of Non - GAAP Financial Measures” slides for more information. 1,030 - 1,080 130 - 166

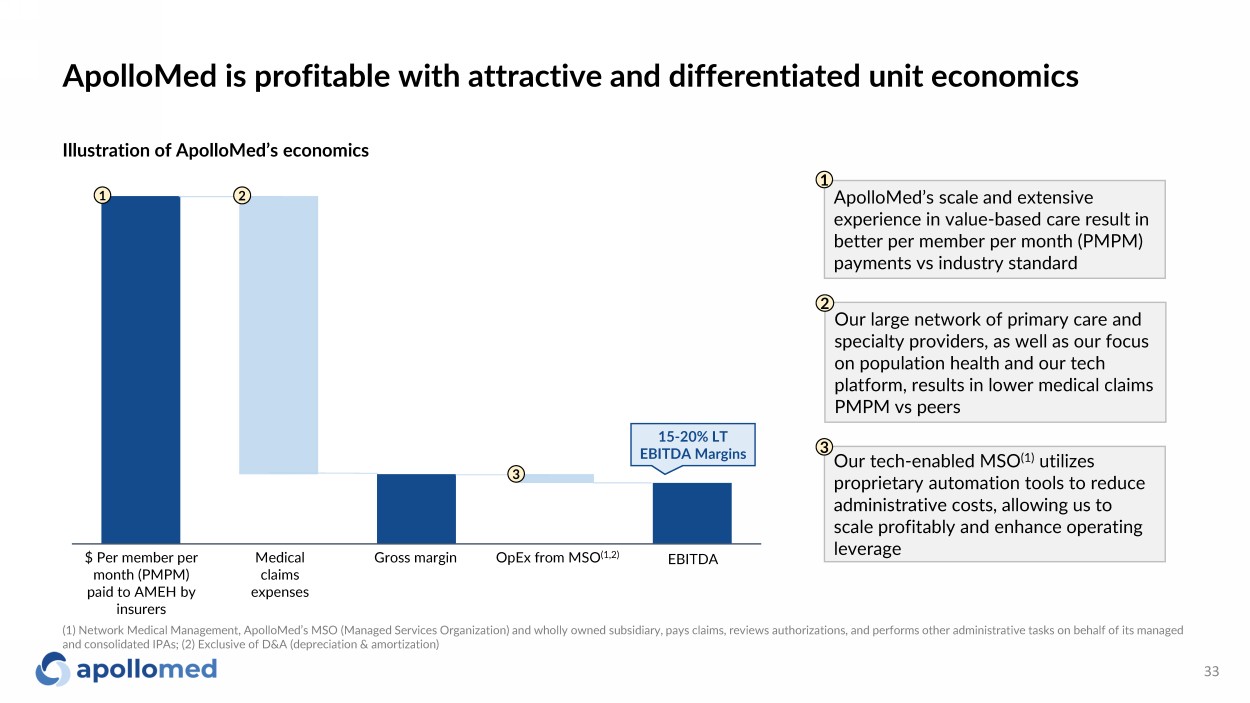

ApolloMed is profitable with attractive and differentiated unit economics 33 1 2 ApolloMed’s scale and e xtensive experience in value - based care result in better per member per month (PMPM) payments vs industry standard 1 Our large network of primary care and specialty providers, as well as our focus on population health and our tech platform, results in lower medical claims PMPM vs peers 2 Our tech - enabled MSO (1) utilizes proprietary automation tools to reduce administrative costs, allowing us to scale profitably and enhance operating leverage 3 $ Per member per month (PMPM) paid to AMEH by insurers Medical claims expenses Gross margin OpEx from MSO (1, 2) EBITDA Illustration of ApolloMed’s economics 15 - 20% LT EBITDA Margins 3 (1) Network Medical Management, ApolloMed’s MSO (Managed Services Organization) and wholly owned subsidiary, pays claims, rev iew s authorizations, and performs other administrative tasks on behalf of its managed and consolidated IPAs; (2) Exclusive of D&A (depreciation & amortization)

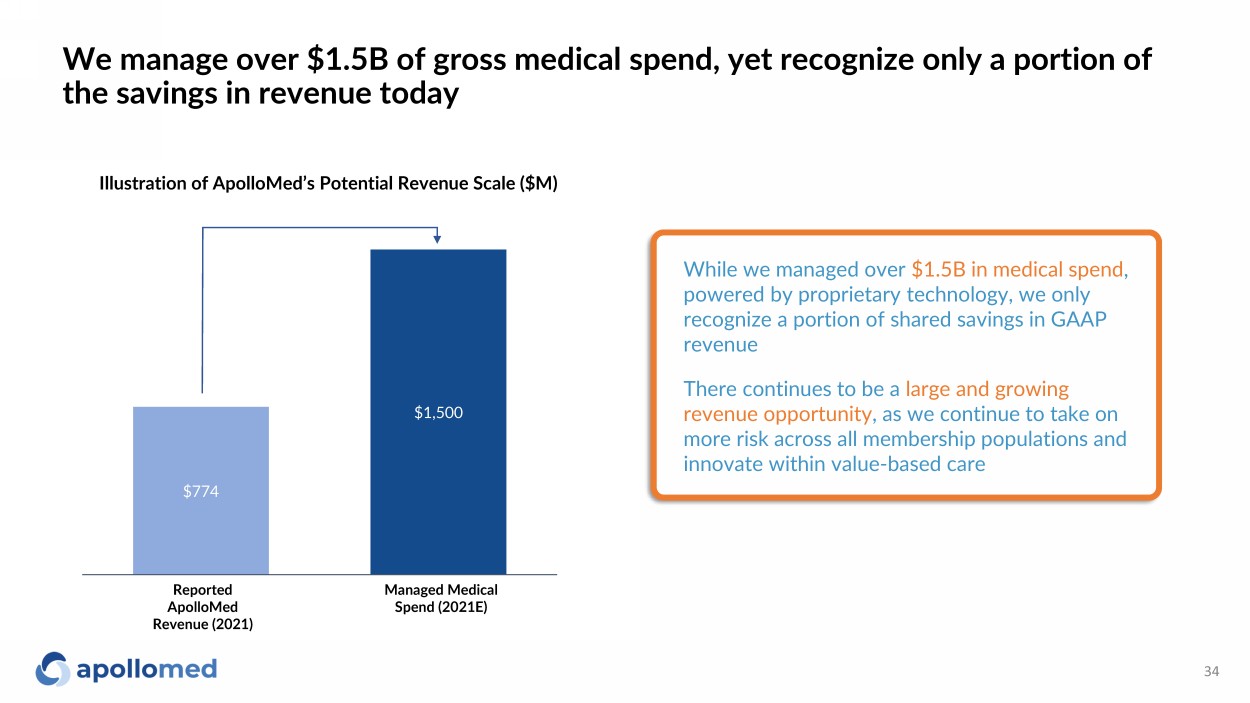

$774 $1,500 We manage over $1.5B of gross medical spend, yet recognize only a portion of the savings in revenue today 34 Illustration of ApolloMed’s Potential Revenue Scale ($M) While we managed over $ 1.5B in medical spend , powered by proprietary technology, we only recognize a portion of shared savings in GAAP revenue Reported ApolloMed Revenue (2021) Managed Medical Spend (2021E) There continues to be a large and growing revenue opportunity , as we continue to take on more risk across all membership populations and innovate within value - based care

Conclusion 35 ApolloMed’s success and experience in value - based care position the company well to capture a growing $2T market across all membership populations With 25+ years of experience, our MSO has a proven track record of handling the challenges that prevent physicians from succeeding in value - based care Combining in - house engineering and value - based care experience, we have built a technology suite to support operational and clinical excellence Our model has produced improvements in clinical outcomes across a wide range of geographies and demographics, showing its scalability ApolloMed’s success in value - based care is validated by a robust financial profile, with both rapidly growing revenue and profitable margins Our management team brings operational, engineering, and clinical expertise to the table, positioning us for continued success in the health care of the future

Appendix

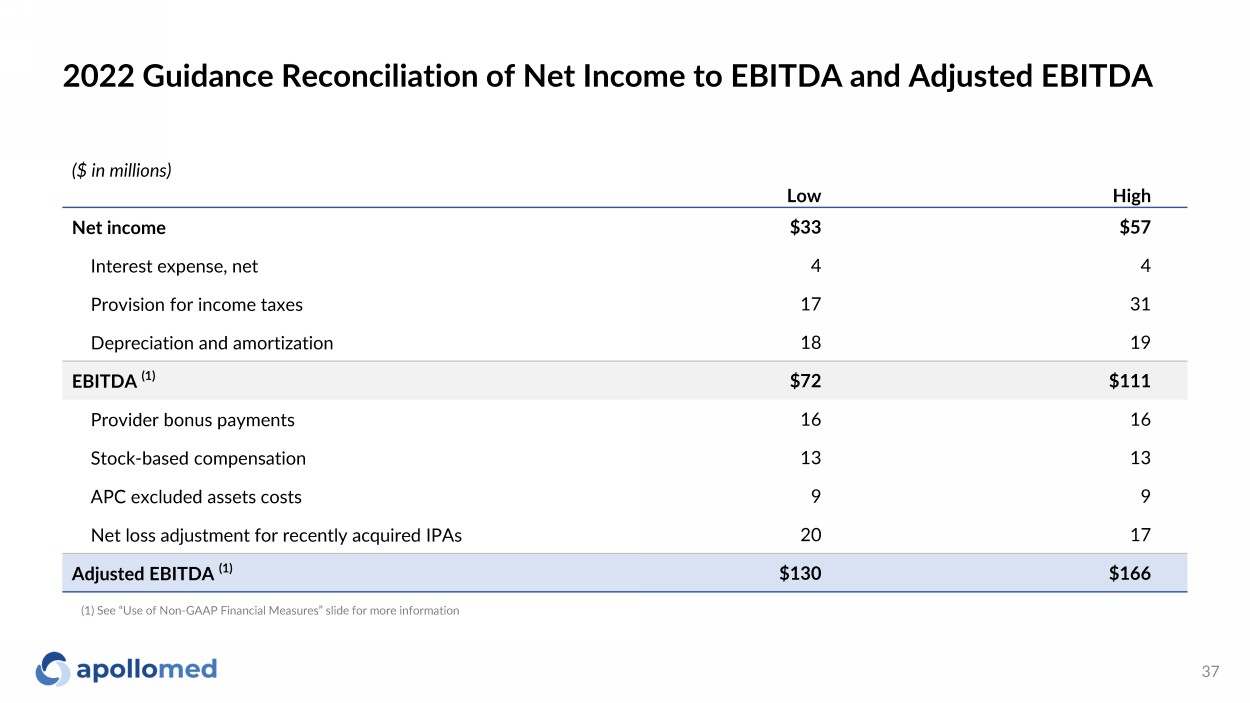

2022 Guidance Reconciliation of Net Income to EBITDA and Adjusted EBITDA 37 (1) See “Use of Non - GAAP Financial Measures” slide for more information ($ in millions) Low High Net income $33 $57 Interest expense, net 4 4 Provision for income taxes 17 31 Depreciation and amortization 18 19 EBITDA (1) $72 $111 Provider bonus payments 16 16 Stock - based compensation 13 13 APC excluded assets costs 9 9 Net loss adjustment for recently acquired IPAs 20 17 Adjusted EBITDA (1) $130 $166

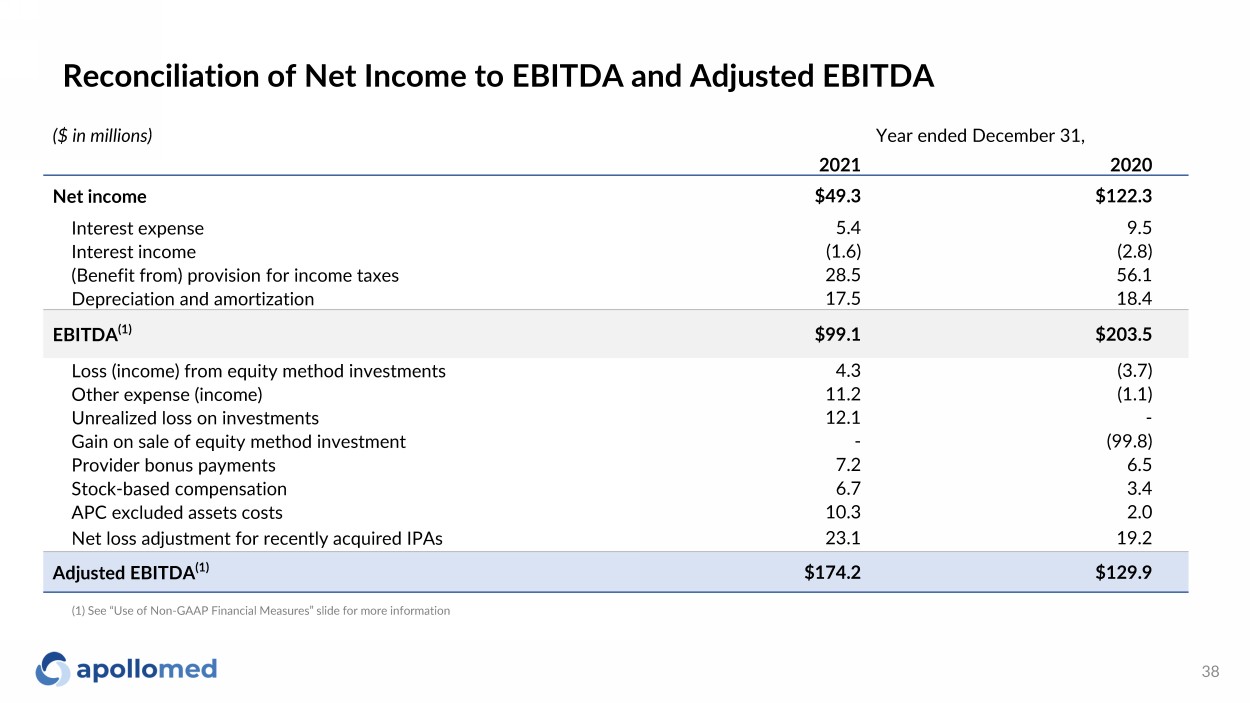

Reconciliation of Net Income to EBITDA and Adjusted EBITDA 38 ($ in millions) Year ended December 31, 2021 2020 Net income $49.3 $122.3 Interest expense 5.4 9.5 Interest income (1.6) (2.8) (Benefit from) provision for income taxes 28.5 56.1 Depreciation and amortization 17.5 18.4 EBITDA (1) $99.1 $203.5 Loss (income) from equity method investments 4.3 (3.7) Other expense (income) 11.2 (1.1) Unrealized loss on investments 12.1 - Gain on sale of equity method investment - (99.8) Provider bonus payments 7.2 6.5 Stock - based compensation 6.7 3.4 APC excluded assets costs 10.3 2.0 Net loss adjustment for recently acquired IPAs 23.1 19.2 Adjusted EBITDA (1) $174.2 $129.9 (1) See “Use of Non - GAAP Financial Measures” slide for more information

Use of Non - GAAP Financial Measures 39 This presentation contains the non - GAAP financial measures EBITDA and adjusted EBITDA, of which the most directly comparable financial measure presented in accordance with U.S. generally accepted accounting principles (“GAAP”) is net (loss) income. These measures are not in accordance with, or an alternative to, GAAP, and may be different from other non - GAAP financial measures used by other companies. The Company uses adjusted EBITDA as a supplemental performance measure of the Company’s operations, for financial and operational decision - making, and as a supplemental means of evaluating period - to - period comparisons on a consistent basis. Adjusted EBITDA is calculated as earnings before interest, taxes, depreciation, and amortization, excluding income from equity method investments, provider bonuses, impairment of intangibles, provision of doubtful accounts, and other income earned that is not related to the Company’s normal operations. Adjusted EBITDA also excludes non - recurring items, including the effect on EBITDA of certain recently acquired IPAs. The Company believes the presentation of these non - GAAP financial measures provides investors with relevant and useful information, as it allows investors to evaluate the operating performance of the business activities without having to account for differences recognized because of non - core or non - recurring financial information. When GAAP financial measures are viewed in conjunction with non - GAAP financial measures, investors are provided with a more meaningful understanding of the Company’s ongoing operating performance. In addition, these non - GAAP financial measures are among those indicators the Company uses as a basis for evaluating operational performance, allocating resources, and planning and forecasting future periods. Non - GAAP financial measures are not intended to be considered in isolation from, or as a substitute for, GAAP financial measures. To the extent this release contains historical or future non - GAAP financial measures, the Company has provided corresponding GAAP financial measures for comparative purposes. The reconciliation between certain GAAP and non - GAAP measures is provided above.

For inquiries, please contact: ApolloMed Investor Relations (626) 943 - 6491 investors@apollomed.net Carolyne Sohn, The Equity Group (415) 568 - 2255 csohn@equityny.com